[ad_1]

Funtay

British American Tobacco (NYSE:BTI) has doubtless disenchanted its holders since BTI topped out in November 2022. I anticipated consumers returning to help the pullback in January, however it has not panned out nicely.

Accordingly, BTI has considerably underperformed the S&P 500 (SPX) (SPY), as BTI re-tested lows final seen in October 2020. As such, I am not stunned that weak holders may have been pushed to throw within the towel and rotate out, regardless of its engaging valuation.

I consider the primary purchase thesis undergirding BTI on the present ranges is undoubtedly its valuation. Looking for Alpha Quant rated an “A+” (very best) valuation grade for BTI. Furthermore, its ahead dividend yield of 8.3% is nicely above its 10Y common of 5.8%.

Nonetheless, regardless of the extremely interesting valuation, consumers have did not return robustly, as promoting strain overwhelmed BTI over the previous seven months. An tried restoration in February 2023 was “torpedoed” as the corporate determined “not to launch a brand new share buyback program.”

Panmure Gordon analysts shared their issues then, suggesting it was “at greatest unusual, at worst disconcerting.” Why so? I believe I can attempt to simplify the logic of inventory buyback, leveraging the knowledge of Warren Buffett from Berkshire Hathaway’s (BRK.A) (BRK.B) latest annual assembly in Might.

Buffett reminded traders that “the decision to repurchase shares may be the dumbest or smartest factor, relying on the circumstances.” He additionally harassed that “if the inventory value is above intrinsic worth, it is a no-brainer to not do a share repurchase program.” Nonetheless, he additionally articulated the “significance of rising the current enterprise and making choices on dividends earlier than contemplating share buybacks.”

As such, I consider that the optics of not shopping for again extra BTI shares within the open market doubtless despatched the incorrect sign to BTI holders that its share was not thought-about “undervalued.” Furthermore, Morningstar applauded administration’s earlier program, because it “created value as a result of the shares have been bought at ranges nicely under [its] truthful worth estimate.”

Nonetheless, I believe the best manner to consider the present state of affairs is that BTI must be even handed about allocating capital within the present macro atmosphere. Is smart?

BTI is coming into arguably probably the most transformative part in its enterprise because it makes an attempt to achieve £5 billion in income for its lowered dangers section by 2025. Nonetheless, that section delivered solely £2.9 billion in income final 12 months. As such, the corporate doubtless must allocate capital aggressively to spend money on the section to make sure it stays on monitor. And there is not any assure of success, because the competitors is intense.

Altria Group’s (MO) buy of NJoy makes an attempt to reshape the market dynamics with Altria’s intensive distribution community. Furthermore, Philip Morris’s (PM) re-entry with iQOS should be fastidiously watched. Therefore, I consider whereas BTI’s dividend security is probably going not in imminent hazard (rated “C-” by Looking for Alpha Quant), the corporate must be cautious, given the continued want to speculate and scale its reduced-risk section.

Subsequently, I am assured that BTI has continued to see enchancment in its reduced-risk merchandise, as the corporate reported just lately that “Vuse value share increased by 2.8 proportion factors, reaching 38.8% in key vapor markets.”

Furthermore, its legacy tobacco section can also be seeing notable enchancment, notably within the premium section. BTI famous sequential development in its premium quantity share “because the starting of the 12 months.”

However, the corporate should nonetheless navigate the secular decline in tobacco merchandise whereas dealing with near-term headwinds within the low cost section. As such, I assessed that market operators have been justified to mirror a wider margin of security towards BTI’s valuation to account for these challenges.

Nonetheless, the query is whether or not these headwinds have been sufficiently accounted for in BTI’s present ranges, permitting dip consumers a possibility to return and take a look at “catch the falling knives?”

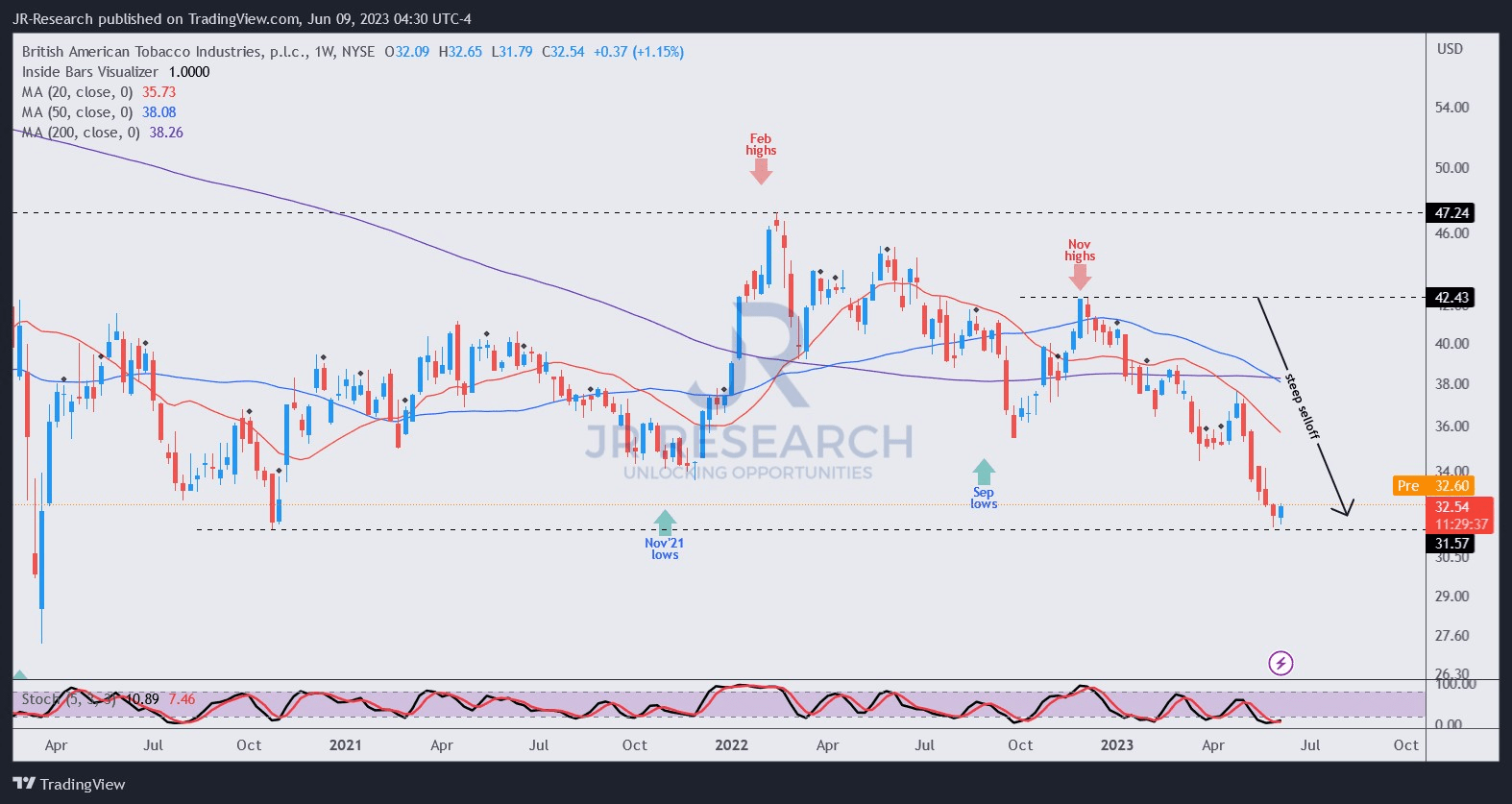

BTI value chart (weekly) (TradingView)

With the steep selloff from BTI’s November highs, I assessed that BTI had reached well-oversold circumstances, permitting for a lower-risk entry level for dip consumers.

Notably, I additionally gleaned that purchasing sentiments have improved over the previous two weeks, corroborated by the discharge of the corporate’s buying and selling replace this week.

Subsequently, given the steep selloff, I consider the chance/reward profile of shopping for the dips on the present ranges is engaging relative to BTI’s threat/reward profile.

Coupled with probably less perilous macroeconomic headwinds transferring forward, a probably sharp mean-reversion alternative to the BTI’s vital transferring averages is more and more doable.

So, it is time to catch the falling knives. As a be aware, I gleaned comparable technical indicators in Warner Bros. Discovery (WBD) inventory in a late May article. Accordingly, WBD has considerably outperformed the SPX over the previous two weeks, notching a acquire of greater than 26% in comparison with the SPX’s 3.4% uptick. Its valuation then was additionally an “A+,” if that rings a bell.

Score: Purchase

Necessary be aware: Buyers are reminded to do their very own due diligence and never depend on the knowledge supplied as monetary recommendation. The ranking can also be not meant to time a selected entry/exit on the level of writing except in any other case specified.

We Need To Hear From You

Have further commentary to enhance our thesis? Noticed a vital hole in our thesis? Noticed one thing necessary that we did not? Agree or disagree? Remark under and tell us why, and assist everybody locally to study higher!

[ad_2]