[ad_1]

Anski

Funding Thesis

With the administration making an attempt to grow to be extra environment friendly over the past couple of years, I needed to take a fast have a look at GameStop’s (NYSE:GME) financials and see whether it is figuring out because the administration deliberate. The corporate remains to be shedding cash left and proper and with no stable trajectory for enhancements, I do not see how this firm could possibly be an funding, aside from being of venture and the loyal “hodlers” who’re nonetheless very lively to this present day. I even determined to make the corporate worthwhile sooner or later in my mannequin and GME remains to be overpriced even then.

The Nostalgia Attraction

To be sincere I get the enchantment of GME. Most people beloved the shop expertise again within the day. I’m one in every of them. Obtained myself a GTA San Andreas again in ’07, though it was rated mature they nonetheless offered it to mini-me, and I beloved that. They most likely simply needed to eliminate a 3-year-old sport by then. I’d go to the shop after faculty to only have a look at the video games there and never purchase them since I used to be broke. Generally I might purchase those that value a couple of euros and would play them continuous for months.

Quick ahead to the current day, and I actually can’t keep in mind the final time I’ve been in a GameStop. I switched in a short time to digital video games, way back to Xbox 360. I nonetheless purchased some video games for the console from GME however as soon as I switched to a PS4, I have never stepped foot within the retailer. And now with the PS5’s respectable storage, quick web, and a less expensive disc-less model, there’s actually no have to go to the shop except I need to get a controller, however even then, I might most likely go to the Amazon retailer (AMZN).

Every time I do stroll by it, I get the nostalgia operating over me certain, however the within the shop hasn’t modified in any respect since after I was a younger lad, it is simply a lot emptier now. The cult following may be very sturdy for the reason that starting of the meme-mania again in Jan-Feb ’21. It died out a little bit, nevertheless, there are nonetheless very lively Reddit pages devoted to GME. I keep in mind in the future a buddy of mine requested the place to speculate, and he mentioned he’s acquired round 100 euros to speculate, then I assumed if that’s all you bought strive GameStop, it’s been on my radar for fairly some time and some months later the meme-mania occurred and it shot as much as over $400 a share, so I referred to as my buddy and requested if he made some huge cash, he 5x his cash, nevertheless, he didn’t make investments the entire 100 euros and he cashed out at round $20 a share, bummer.

Outlook

The corporate has been making an attempt a bunch of various issues to remain related, however nothing has actually labored. The promoting of Funko Pops and different collectibles, was the one income section to see a good progress y-o-y, whereas {hardware} gross sales have been down 1% and software program gross sales have been down 9%. It is even making an attempt to leap into the e-sports scene, which has been bleeding cash additionally.

The corporate goes to try to pivot again to brick-and-mortar stores. It should do a number of work on that entrance and shut down many extra shops to grow to be worthwhile and extra environment friendly as a result of proper now, there are method too many shops which are shedding cash. The plan is to make use of these shops as “mini achievement facilities” for e-commerce ventures that the present Chairman of the corporate Ryan Cohen was aggressively making an attempt to pivot to.

The objective is to streamline operations and grow to be worthwhile. Will this work? We should look forward to fairly some time earlier than we see any outcomes, but when the previous is a sign, scrambling to make the corporate worthwhile didn’t work, so I am undecided how effectively it will work both.

Financials

It is all the time essential to take a look at the corporate’s insides to see the way it carried out previously, which can point out the place it is going sooner or later. Spoiler alert, it is not wanting too good for GME on this entrance.

Positive, the money and debt place has improved over the past couple of years. That, at most, will give the corporate a couple of years of survivability if it’s going to maintain shedding cash yearly because it has. Money and little or no leverage are nice for firms. It offers them the flexibleness to pursue new ventures as GME has previously, with little success to date, nevertheless, one thing would possibly finally stick, so I’d say go for it!

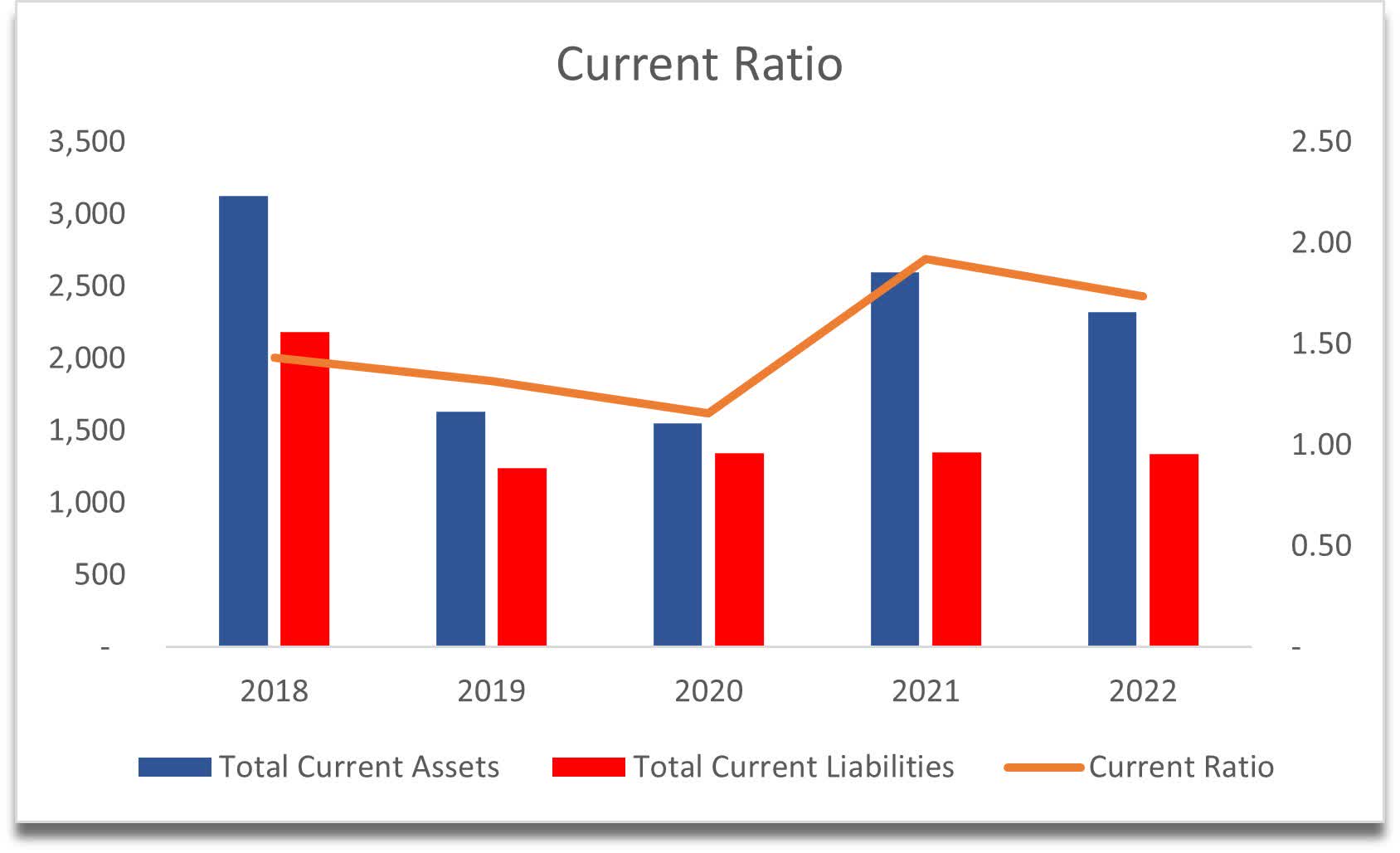

The corporate’s present ratio is respectable sufficient, which suggests it has no points paying off its short-term obligations. So, it could keep afloat a little bit longer.

Present Ratio (Personal Calculations)

The large deal for the corporate is profitability and effectivity. Within the newest earnings name, which by the best way, was the shortest I’ve heard to date, Matt Furlong mentioned the corporate goes to be very aggressive in reducing prices in ’23, particularly in Europe. He was very decided to chop prices aggressively on the decision. That is a great signal certain, however since we haven’t any concrete proof of it occurring but, we should wait till subsequent 12 months to see what number of have been lower and the way a lot of an enchancment the corporate noticed by way of effectivity.

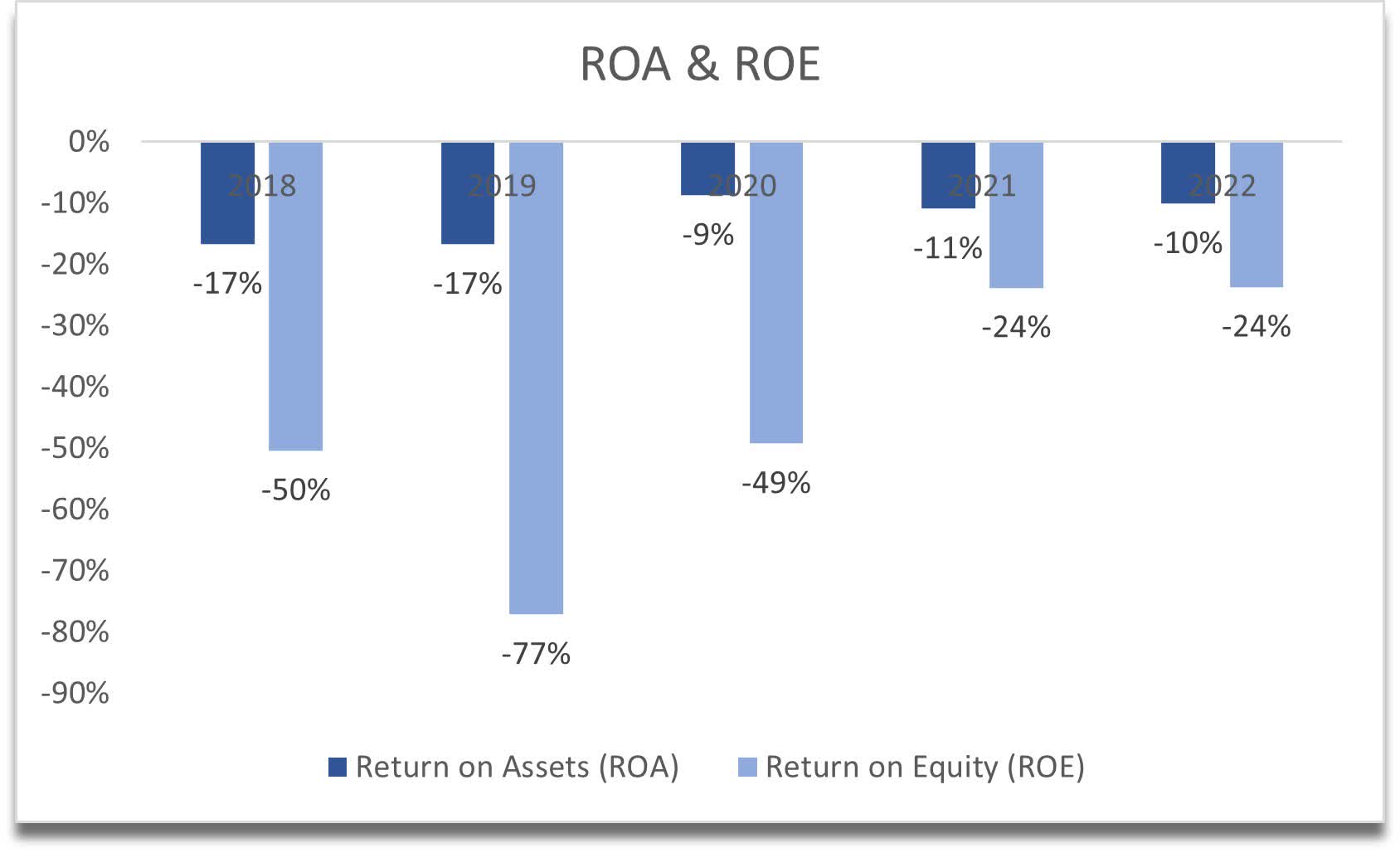

On the finish of FY22, the corporate’s ROA and ROE have been abysmal, to say the least. Perhaps one optimistic factor I might say about these metrics is that they don’t seem to be as dangerous as they have been in ’19. If I used to be a “hodler” I might be this as a really optimistic signal for the inventory, simply saying. To a impartial particular person, this simply tells me that the corporate is not using its property and shareholders’ capital effectively.

ROA and ROE (Personal Calculations)

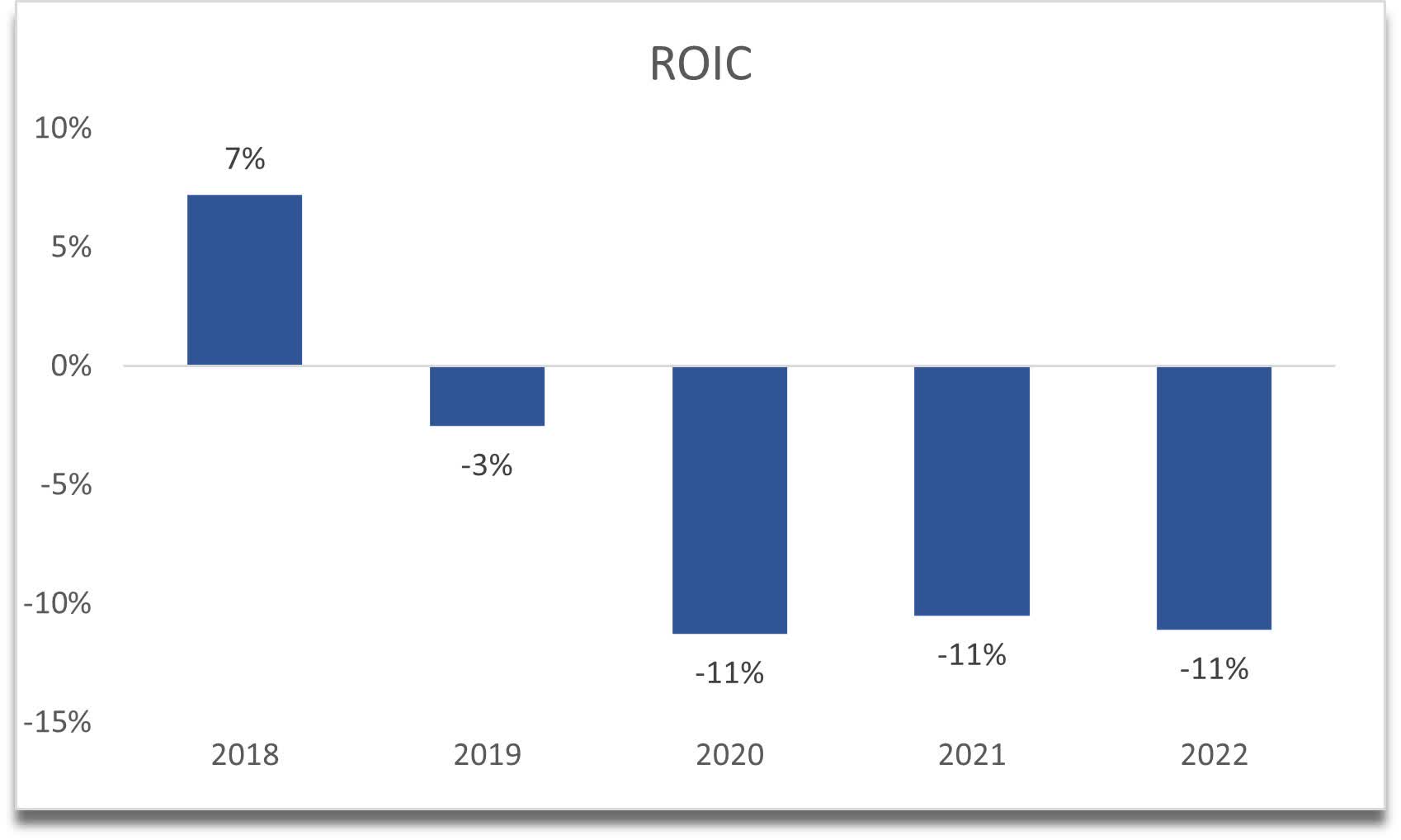

When it comes to return on capital invested, it has been fairly terrible too. The aggressive benefit that the corporate could have had previously is gone and digitization has been successful. The moat has deteriorated in my opinion.

ROIC (Personal Calculations)

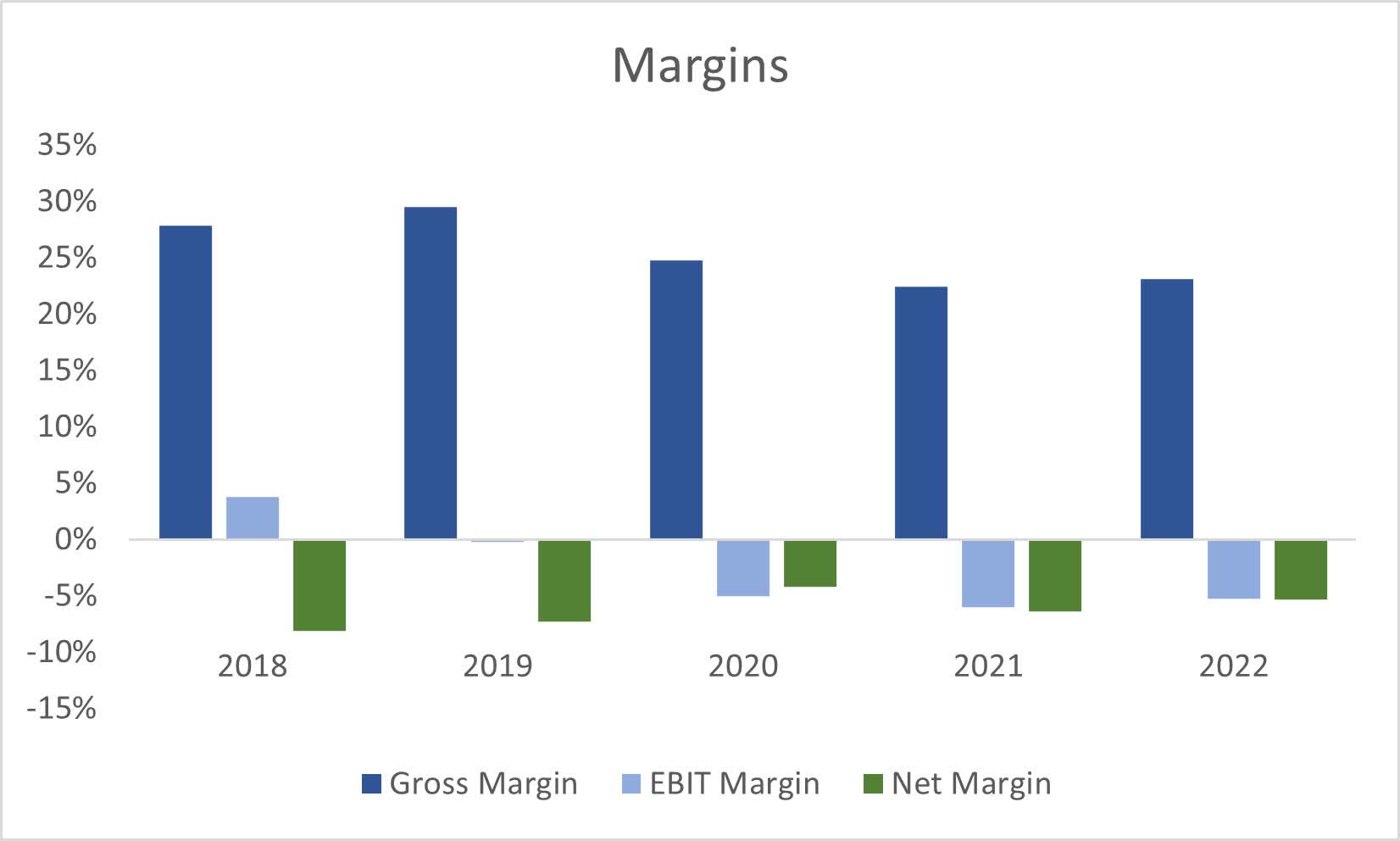

When it comes to margins, it is not wanting good both. These have been taking place persistently yearly, that means that the initiatives that the corporate had previously didn’t work in any respect, and it is no marvel they’ve all been scrapped. If the aggressive cost-cutting measures work sooner or later, it’s doable to show the ship round, nevertheless, it’s going to take a very long time earlier than we see some outcomes.

Margins (Personal Calculations)

General, I see an organization that’s been on the point of extinction and if nothing works out within the close to future, I believe it could possibly be going the best way of the Dodo and Blockbuster. I’ve coated a few huge gamers of the previous that managed to pivot their enterprise fully like Nokia (NOK), so I wish to see GME discovering the right combination of merchandise that may make it grow to be a viable firm but once more.

Valuation

To be sincere, the one method of an organization’s valuation right here can be by way of an optimistic lens. I will assume the corporate manages to show round and enhance margins considerably whereas conserving income progress at round 5% CAGR for the following decade, I simply don’t see it rising any greater than that, particularly because it’s been shedding income yearly aside from a slight bounce in ’21.

For the bottom case, 5% CAGR till ‘32 remains to be optimistic. To go even additional, the optimistic case CAGR is 9%, and the conservative case is 3%.

When it comes to margins, I’m going to imagine the aggressive value measures labored and gross margins improved by a whopping 15% over the following decade. I additionally barely improved working margins by round 400bps, or 4% within the subsequent decade.

I’m additionally going to offer a a lot bigger margin of security than I normally do. 45% will probably be enough I’d say.

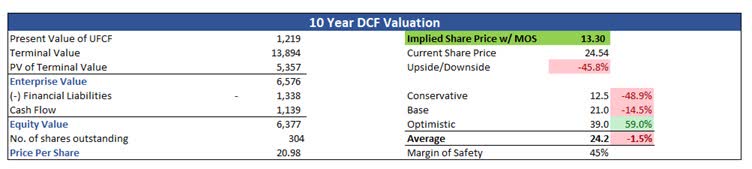

With these very optimistic assumptions, the corporate’s intrinsic worth is $13.30 a share, implying a forty five% draw back from present valuations.

Optimistic Intrinsic Worth (Personal Calculations)

A practical case just isn’t even value doing for my part, as it will imply the corporate ought to technically be out of enterprise. I normally wish to maintain it conservative, however conservative wouldn’t work on this case.

Closing Feedback

If the basics of the corporate don’t enhance over the following couple of years, I actually don’t know the way it’s going to outlive for very lengthy. Earnings are scheduled to be on June 7th, and I’m assuming it’ll be a fast one but once more. I wish to hear extra in regards to the firm’s aggressive cost-cutting measures and enhancements in margins to see whether it is on course.

At this level, the corporate is a promote for certain, however I am certain whoever has shares within the firm will not be promoting them any time quickly. It is fairly low-cost to carry on to it, within the hopes of one other random rally that we might even see after earnings, which if it happens, I consider will dwindle once more because it normally does.

It is my perception that fundamentals don’t drive the share value on this case. It’s the merchants and fanatics. Even the slightest excellent news can propel the share value. Choices premiums aren’t as juicy as they’ve been however every now and then it’s doable to promote a few name or put choices for a good premium and look forward to that IV crush, however that is a really dangerous technique in the case of meme shares.

I will test on the corporate’s standing every now and then however is not going to be following it very intently. If the corporate goes to show the ship round, it is not going to be in a single day.

[ad_2]