[ad_1]

pandemin

A visitor publish by D Coyne

The EIA’s Short-Term Energy Outlook (STEO) was revealed in early Might. The report that follows compares World Petroleum Liquids output from the STEO with estimates from OPEC’s Month-to-month Oil Market Report (MOMR) from May and the IEA’s Oil Market Report (OMR) from February 2023 with an replace on World liquids output primarily based on the abstract of the May report with my estimate on quarterly output in 2023 primarily based on the annual estimate for 2023 revealed in Might 2023 and the quarterly numbers revealed in February 2023.

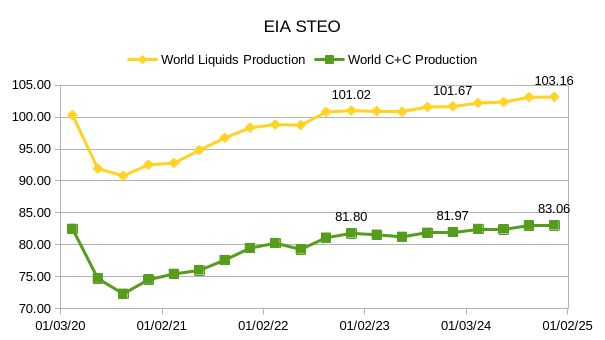

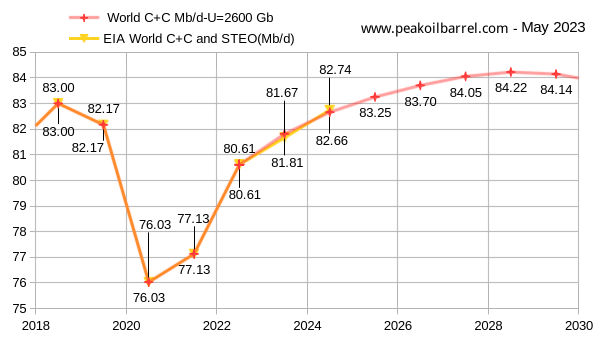

Determine 1

Within the chart above, I modified the EIA Liquids estimate from 2023Q2 to 2023Q4 by assuming that the OPEC crude output matches the decision on OPEC for these months. This assumption reduces the 2024 annual output for World C+C to about 82.74 Mb/d from the STEO estimate of 82.94 Mb/d.

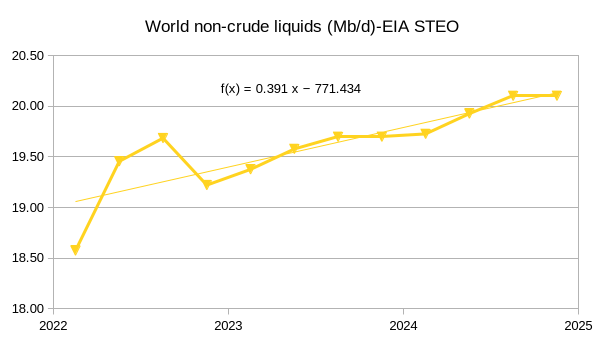

Determine 2

The chart above reveals the rise within the hole between World liquids and World C+C from 2022 to 2024, which I name non-crude liquids (largely NGL, but additionally biofuels equivalent to ethanol and biodiesel, and refinery features).

The speed of enhance primarily based on OLS on the information within the chart is 391 kb/d per 12 months. A lot of this enhance might be from the US, which has growing Pure Gasoline and NGL output.

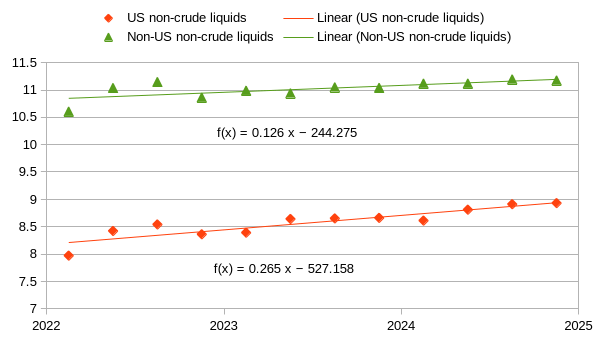

Determine 3

The chart above confirms that about 68% of the rise in World non-crude liquids comes from the US primarily based on the EIA estimates within the STEO.

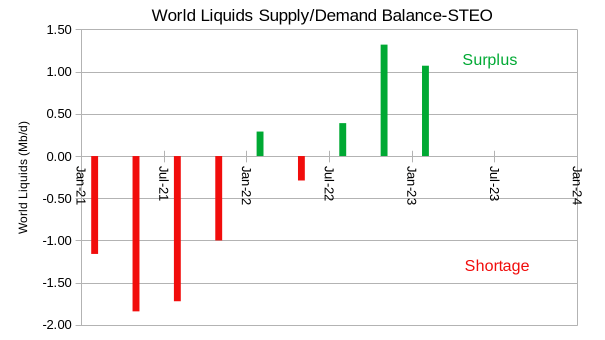

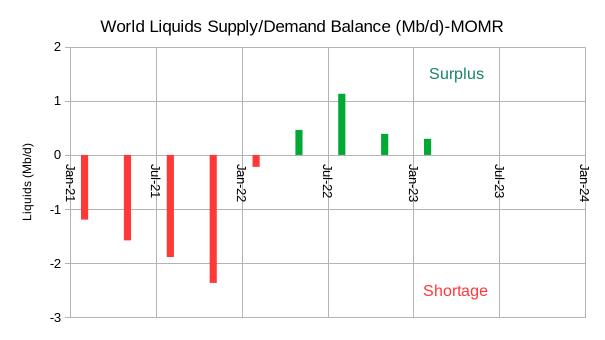

Determine 4

Determine 4 above reveals the stability of provide and demand for World Liquids by means of 2023Q1. Past this, I’ve assumed OPEC acts as a swing producer and tries to stability provide and demand on World markets.

Thus, there isn’t a surplus or scarcity on the World market after 2023Q1, if OPEC chooses the EIA Non-OPEC provide and World demand estimates as the idea for its output.

Determine 5

The chart above considers the World Liquids provide and demand stability primarily based on OPEC’s estimates for World provide and demand. As earlier than, we assume OPEC chooses to fulfill the decision on OPEC in order that after 2023Q1, there isn’t a surplus or scarcity.

I don’t present an identical chart for the IEA OMR as a result of the information is 3 months previous. I can’t assemble this sort of chart for Might as a result of I can’t entry the complete Might Oil Market Report from the IEA.

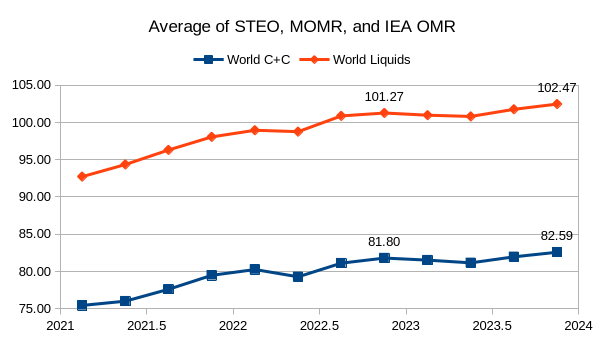

Determine 6

The chart above takes the common of the EIA STEO, OPEC MOMR, and my estimate for the IEA OMR for Might for World liquids. It makes use of an identical methodology as was used for the STEO to assemble an estimate of World C+C primarily based on the EIA’s International Energy data for World C+C and the ratio of World minus US C+C to liquids ratio for 2022.

When evaluating with determine 1 word that the horizontal scales are completely different and that the 82.59 Mb/d for 2024Q4 in determine 6 ought to be in contrast with the 81.97 Mb/d estimate for a similar quarter in Determine 1.

In brief, the EIA estimate is essentially the most conservative of the three companies for his or her 2023 estimate for World C+C (for 2023 annual output EIA is 81.67 Mb/d vs 81.81 for the three company common).

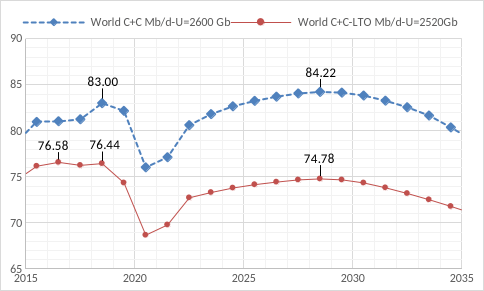

Determine 7

The chart above makes use of Paul Pukite’s Oil Shock Mannequin to estimate future output with the belief {that a} transition to electrical transport reduces oil demand to lower than provide by 2035 (+/- 2 years).

The info above the road is EIA knowledge as much as 2022 and 2023 and 2024 are the STEO estimates, the information under the road is the mannequin output. The 2018 peak is exceeded in 2025 for my finest guess mannequin (100% chance this will likely be unsuitable) and the height is in 2028 at 84.2 Mb/d.

Determine 8

The chart above reveals the quantity of distinction tight oil has made to the World Oil Market, World C+C much less tight oil peaked in 2016. A brand new peak is simply reached in 2028 as a consequence of elevated tight oil output from 2018 to 2028. That is the rationale I concentrate on tight oil.

Determine 9

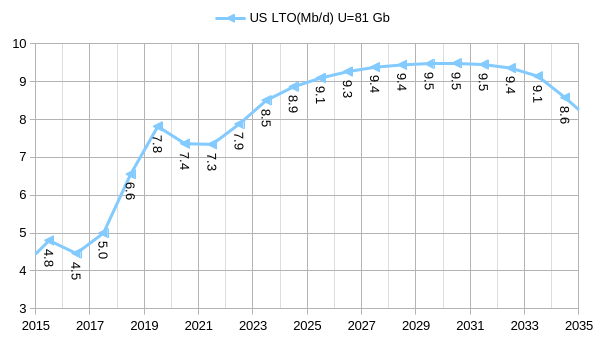

The chart in determine 9 reveals the tight oil mannequin utilized in my Oil Shock Mannequin in determine 7. Output peaks in 2029 and is roughly on plateau from 2027 to 2032. The info proven on the chart is common annual output in hundreds of thousands of barrels per day. Be aware that on the peak in 2018, tight oil output was solely 6.6 Mb/d. I’ll cowl future tight oil output in better element under.

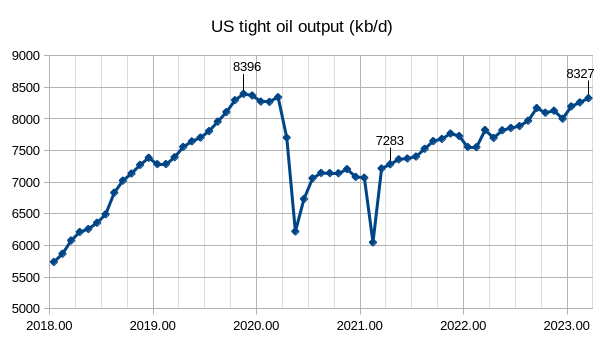

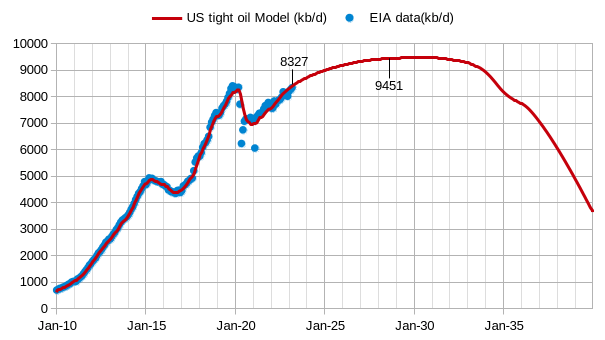

Determine 10

Determine 10 offers an outline of US tight oil output primarily based on EIA Official estimates. The height was November 2019 at 8396 kb/d. In March 2023, output had reached 8327 kb/d some 69 kb/d under the height.

In April 2021, output was 7283 kb/d so the straightforward straight line enhance over two years was 1044 kb/d or 522 kb/d per 12 months. Be aware the distinction within the slope of the road from Jan 2018 to Dec 2019 vs. April 2021 to March 2023, roughly a 2.5 occasions steeper slope within the earlier 2018-2019 interval.

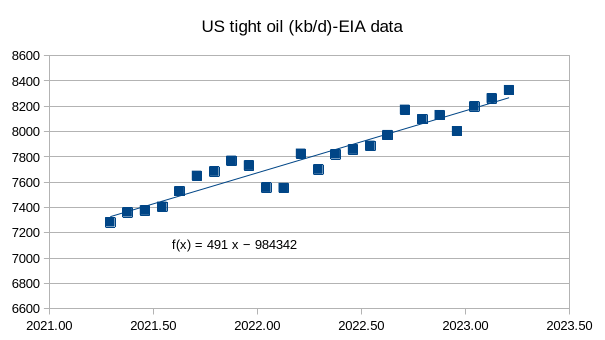

Determine 11

The precise annual price of enhance is healthier measured utilizing an OLS pattern and in determine 11 we see that that is about 491 kb/d per 12 months over the April 2021 to March 2023 interval for US tight oil.

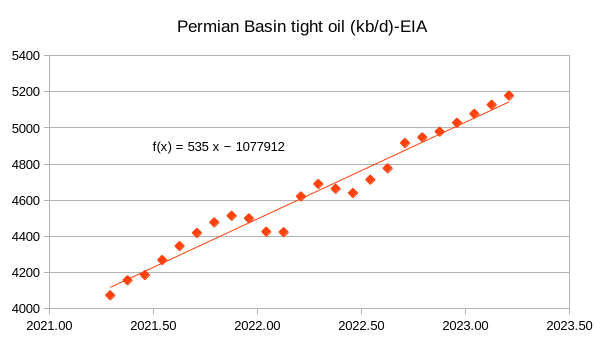

Determine 12

For the Permian basin, the annual price of enhance was 535 kb/d per 12 months from April 2021 to March 2023.

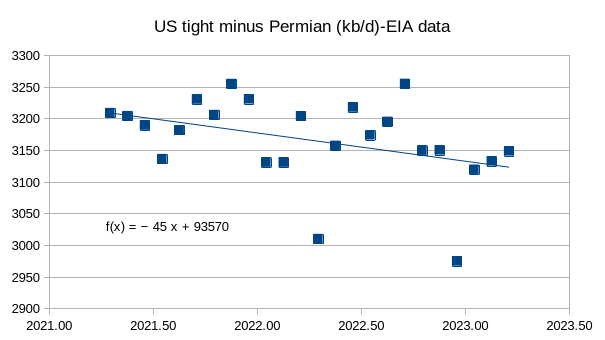

Determine 13

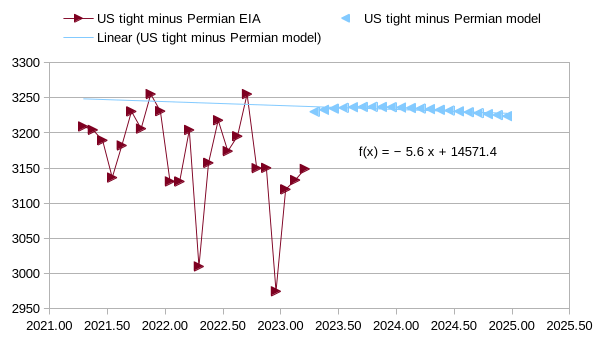

For US tight oil minus Permian tight oil, the speed of lower in annual output was 45 kb/d per 12 months.

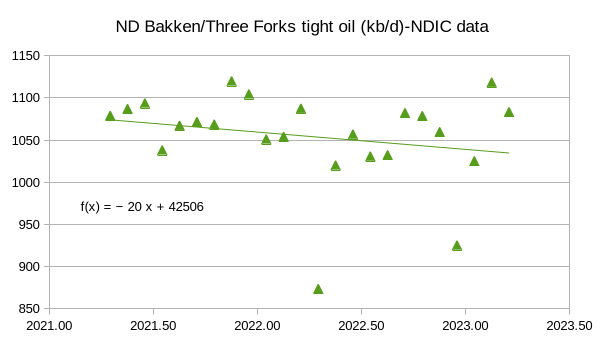

Determine 14

For the North Dakota Bakken I exploit NDIC (North Dakota Industrial Fee) knowledge in determine 14. Common annual output decreased by 20 kb/d per 12 months over the previous 2 years.

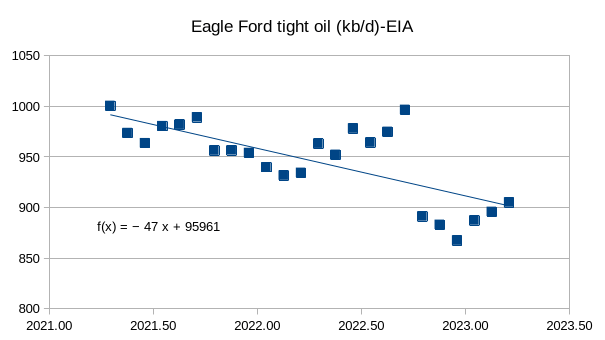

Determine 14

The chart above appears to be like like there could also be an issue with the latest 6 months of information, there have been a variety of revisions recently to EIA knowledge and this appears to be like suspicious to me. In any case, the pattern is a lower of 47 kb/d per 12 months over the previous 2 years.

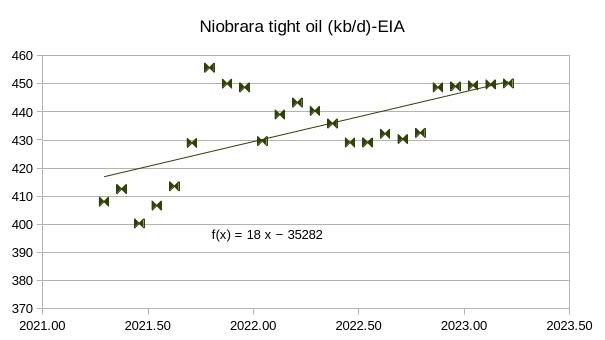

Determine 15

The info for the latest 5 months for the Niobrara additionally appears to be like anomalous, however the pattern is a rise of 18 kb/d over the previous 24 months.

Determine 16

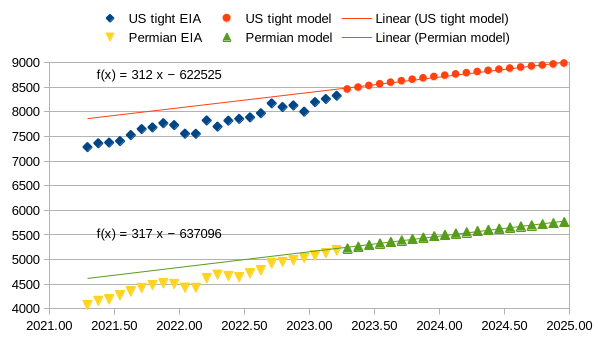

The chart above reveals projected output for a situation the place the completion price for US tight oil wells stays fixed on the March 2023 degree till December 2024. US tight oil will increase at an annual price of 312 kb/d from April 2023 to December 2024 and Permian output will increase at an annual price of 317 kb/d over the identical interval.

Determine 17

The chart above reveals the lower in non-Permian US tight oil output for my finest guess fashions. My expectation is that the latest 3 months of information will likely be revised greater sooner or later, probably the mannequin is about 50 kb/d too excessive. Annual output decreases at about 6 kb/d per 12 months over the April 2023 to Dec 2024 interval.

Determine 18

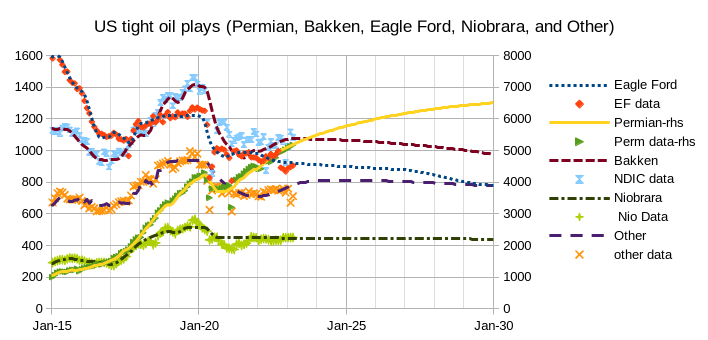

Be aware that the eventualities above assume no enhance within the completion price after March 2023; it stays fixed from April 2023 to December 2029. The Permian mannequin and knowledge ought to be learn on the right-hand vertical axis; all different performs are learn from the left hand vertical axis. Permian situation URR is 51.7 Gb, Bakken URR is 9.2 Gb, Eagle Ford URR is 8.5 Gb, Niobrara URR is 3.5 Gb, and Different tight oil URR is 7.6 Gb.

Determine 19

The chart above merely is the sum of the eventualities offered in Determine 18. I lengthen the chart out to 2039 simply to point out that I do anticipate output to say no pretty rapidly falling by half in 5.33 years from 9000 kb/d in Jan 2034 to 4500 kb/d in April 2039.

The URR of the tight oil situation is about 81 Gb. The common annual price of enhance from March 2023 to July 2028 is about 2.4% per 12 months for this situation.

Editor’s Be aware: The abstract bullets for this text have been chosen by Searching for Alpha editors.

[ad_2]