[ad_1]

Month-to-month indicators of employment, consumption, private earnings (ex-transfers) are all rising in April. However GDO and GDP+ present a decline for 2022Q4 and 2023Q1.

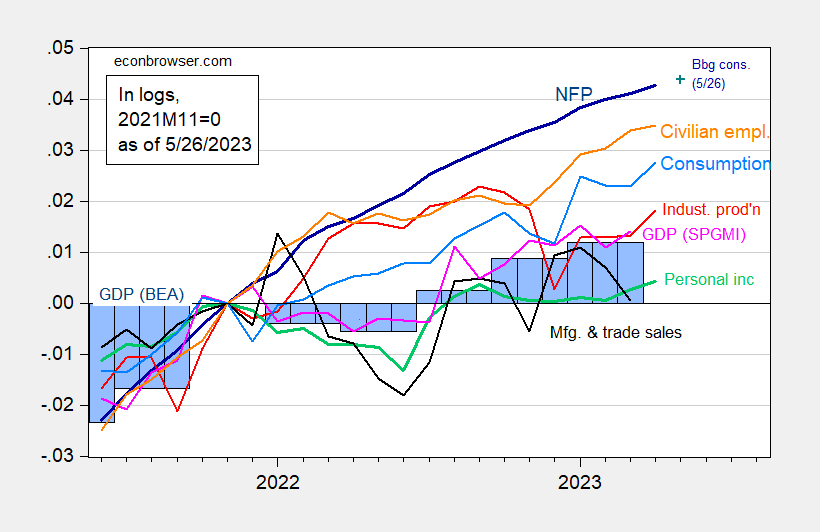

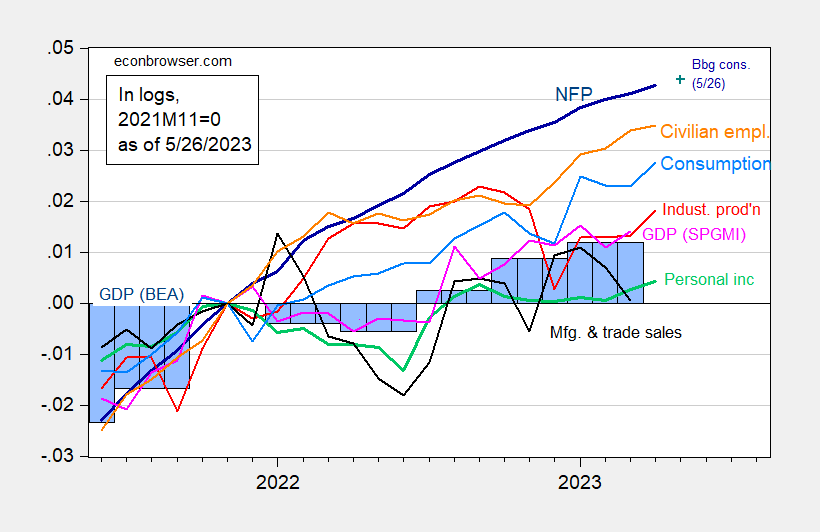

Determine 1: Nonfarm payroll employment, NFP (darkish blue), Bloomberg consensus of 5/26 (blue +), civilian employment (orange), industrial manufacturing (pink), private earnings excluding transfers in Ch.2012$ (inexperienced), manufacturing and commerce gross sales in Ch.2012$ (black), consumption in Ch.2012$ (mild blue), and month-to-month GDP in Ch.2012$ (pink), GDP (blue bars), all log normalized to 2021M11=0. Bloomberg consensus stage calculated by including forecasted change to earlier unrevised stage of employment accessible at time of forecast. Supply: BLS, Federal Reserve, BEA 2023Q1 2nd launch by way of FRED, S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (5/1/2023 launch), and creator’s calculations.

Given the NBER Enterprise Cycle Courting Committee’s emphasis on employment and private earnings, one can be pretty assured that no recession was in place as of April 2023, after all maintaining in thoughts all these numbers can be revised over time. GDP specifically can be revised quite a few instances so a rise on this sequence wouldn’t be decisive in ruling out a recession (simply because the decline in 2022Q1-Q2 wouldn’t be decisive in ruling in a recession).

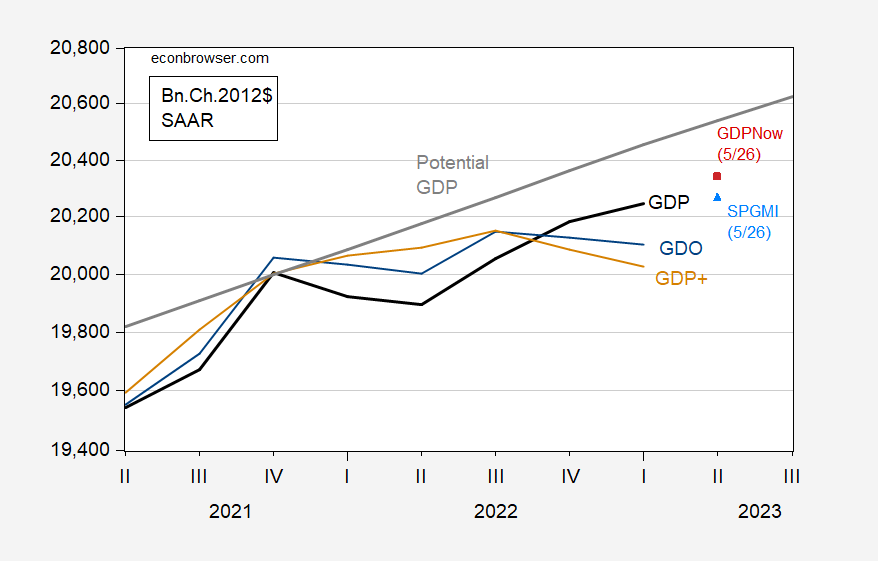

We all know that reported GDP is definitely not the perfect indicator of the place GDP will finally be revised to. GDO and GDP+ are two sequence usually tend to fulfill that situation. Right here, we see some troubling indicators.

Determine 2: GDP (black), GDO (blue), GDP+, scaled to 2019Q4 (tan), potential GDP (grey line), GDPNow of 5/26 (pink sq.), SPGMI monitoring of 5/26 (sky blue triangle) in bn.Ch.2012$ SAAR. Supply: BEA, Philadelphia Fed, CBO (February 2023), Atlanta Fed, S&P International Market Insights, and creator’s calculations.

Whereas GDP was revised as much as 1.3% SAAR, GDO (the typical of GDP and GDI) and GDP+ are at -0.5% and -1.2% SAAR, respectively. As Jason Furman has famous, the discrepancy between GDP and GDI may be very giant, highlighting the uncertainty we face discerning how financial exercise trending. This reveals up in a discrepancy within the bean counting workouts, with GDPNow at 1.9% SAAR, however SPGMI (previously Macroeconomic Advisers and IHS Markit) at 0.4% — primarily zero.

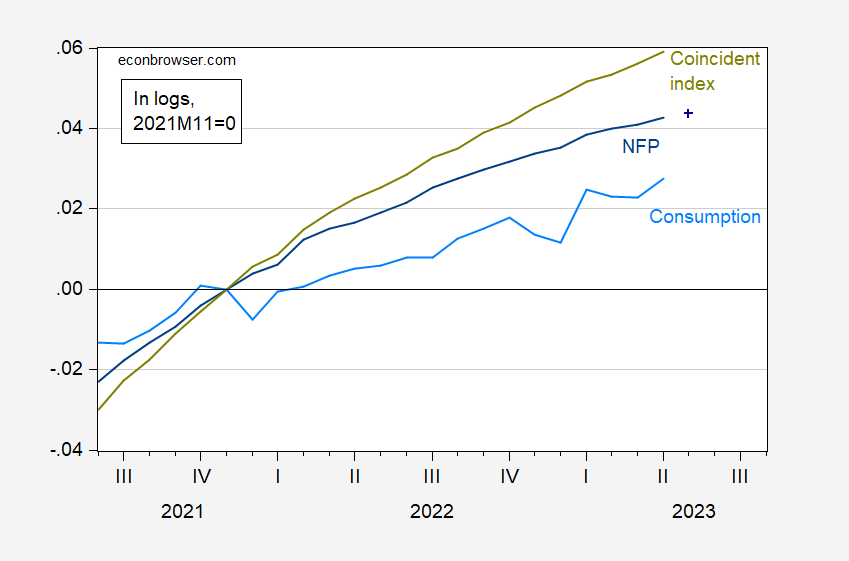

As Furman notes, if GDP and GDI have been the one sequence we noticed, we’d look to GDO. However, to emphasize once more, we have now a lot of proof concerning the power of the labor market. One abstract measure is the Philadelphia Fed coincident index for the US. In Determine 3, I present the coincident index, in comparison with nonfarm payroll employment, and to consumption.

Determine 3: Coincident index (chartreuse), nonfarm payroll employment (blue), Bloomberg consensus of 5/26 (blue +), consumption (sky blue), all in logs, 2021M11=0. Supply: Philadelphia Fed, Bloomberg, BLS and BEA by way of FRED, and creator’s calculations.

The coincident index relies on largely labor market indicators, and has repeatedly elevated, even throughout 2022H1, when some observers argued {that a} recession had arrived. Consumption, which is usually sustained by wage and wage funds, has additionally largely risen over the past yr and half, and suprised on the upside in April.

So, in sum, uncertainty reigns!

[ad_2]