[ad_1]

No matter gross or internet, at par or market worth, as a ratio to GDP or potential GDP, the reply is fairly apparent.

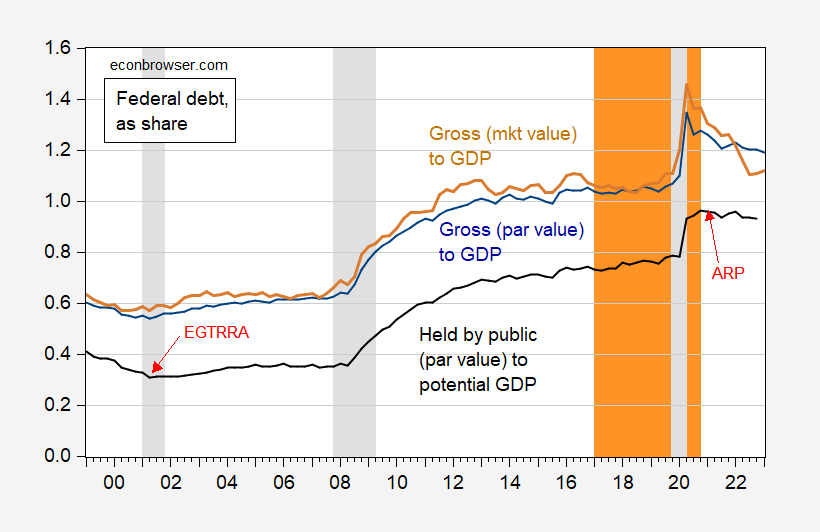

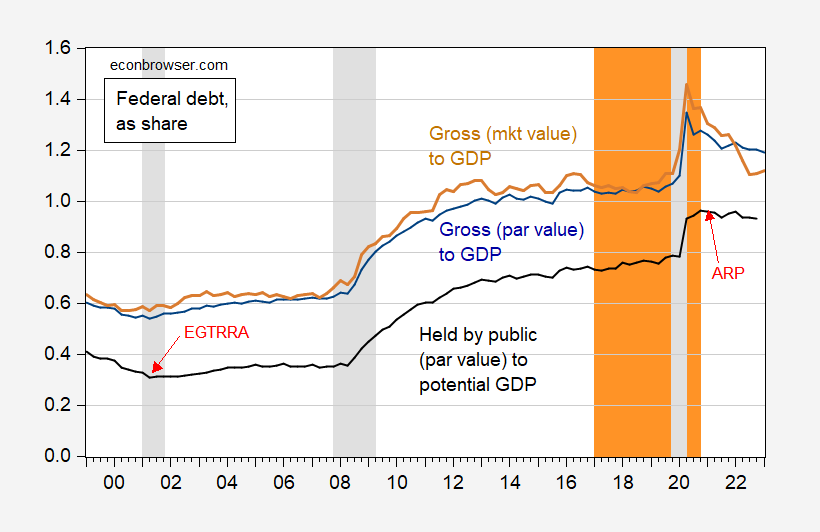

Determine 1: Gross Federal debt at par worth as ratio of GDP (blue), at market worth as ratio to GDP (tan), Federal debt held by public at par worth as ratio to CBO potential GDP (black). NBER outlined peak-to-trough recession dates shaded grey. Trump administration shaded orange. Supply: Treasury by way of FRED, Dallas Fed, CBO (February 2023), NBER, and creator’s calculations.

Publicly held debt as a share of potential GDP rose by 15 proportion factors going from 2020Q1 to 2020Q2. The 25 ppts improve utilizing precise GDP is in some sense deceptive as a result of it’s largely by the sharp drop in output in Q2.

The market worth of debt has dropped considerably greater than the par worth, and in some methods the market worth is extra consultant of the burden posed by the excellent inventory of debt (see dialogue here).

None of this could detract from the argument that the trail of debt isn’t sustainable. I’d say that it’s unattainable, given the consensus to take care of protection and Social Safety, to meaningfully tackle this drawback with out elevating extra income. (Productiveness and output enhancing measures, like elevated immigration, wouldn’t harm both.)

(Facet Word: Japan’s internet debt to GDP in 2021 was about 170%).

[ad_2]