[ad_1]

MundusImages/E+ through Getty Pictures

We’re downgrading Apple Inc. (NASDAQ:AAPL) to a promote regardless of the stronger-than-expected iPhone gross sales in fiscal Q2 2023 that saved the day. Whereas we anticipate Apple is en path to get well from post-pandemic lows, we anticipate restricted upside within the close to time period and see favorable exit factors at present ranges.

Apple inventory is buying and selling at roughly $173 per share, extremely near its 52-week-high of $176.15, and buying and selling effectively above the peer group on each P/E and EV/Gross sales metrics. iPhone gross sales are up, signaling that the smartphone market could stabilize after a rigorous wave of weaker client spending and up to date stock correction cycles. Nevertheless, we imagine it’s too early to say we’ve exited the smartphone contraction section of the post-pandemic setting; we forecast the smartphone complete addressable market, or TAM, to contract this yr by round 2.5% compared to 2022, concurrently Canalys reported world smartphone market “skilled its fifth consecutive quarter of decline, falling by 13% Y/Y in 1Q23” and IDC reported worldwide shipments dropped 14.6% Y/Y in the identical quarter.

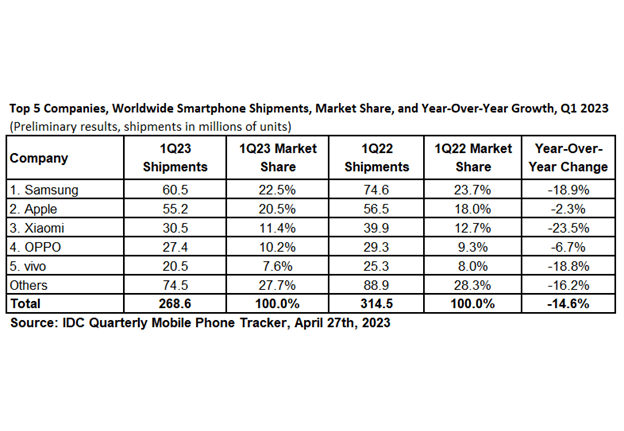

iPhones nonetheless make up the majority of Apple’s revenues; therefore, whereas the smartphone market seems to be stabilizing, this gained’t occur in a single day. The smartphone market is at the moment in oversupply; therefore, regardless of the better-than-expected iPhone gross sales, we anticipate a correction to happen within the close to time period. With this stated, Apple might additionally leverage the chance to outperform consensus extra simply, because the oversupply within the semiconductor business and macro headwinds create softer consensus expectations. The corporate’s put in base can be superior to the competitors within the smartphone market, enabling Apple to maintain gross sales with much less danger and with out giving into aggressive pricing. The next chart outlines the highest smartphone corporations’ market share in 1Q23.

IDC

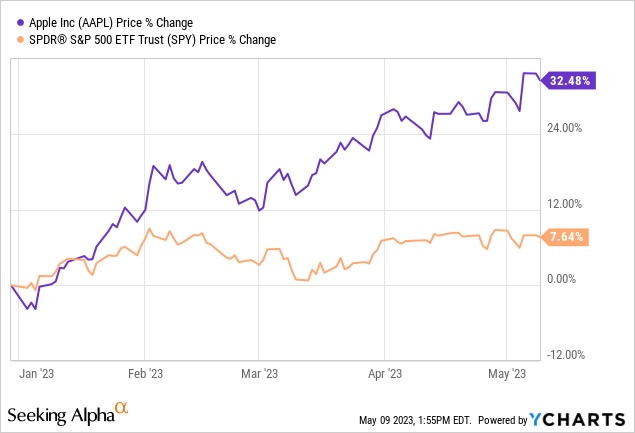

Because it stands, the corporate’s market share is 20.5%, with smartphone shipments dropping 2.3% Y/Y, in comparison with Samsung Electronics Co., Ltd. (OTCPK:SSNLF), with a 22.5% market share and shipments dropping 18%. We don’t see the corporate’s share increasing within the close to time period and imagine there might be a window to build up at extra favorable ranges additional into 2H23 earlier than Apple’s share expands extra meaningfully. The inventory is up roughly 33% YTD, outperforming the S&P 500 (SP500) by almost 25%. Apple is best positioned than it was a yr in the past to outperform, however we see the most effective plan of action is counting income at present ranges, exiting the inventory, and revisiting as soon as the inventory drops nearer to the $150s vary.

The next chart outlines Apple inventory in opposition to the S&P 500 YTD.

YCharts

Q2 2023 & What’s Subsequent

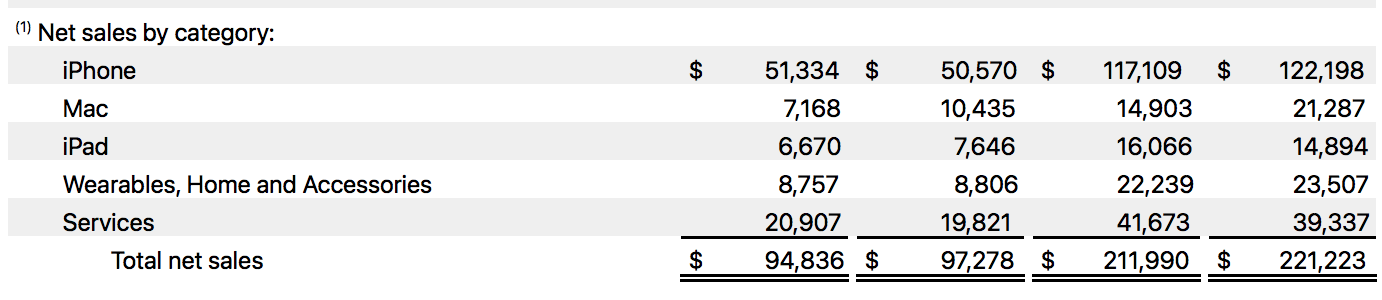

Apple reported 2Q23 earnings beating prime and backside traces this quarter; GAAP EPS of $1.52 and income of $94.84B, down barely 2.5% Y/Y. iPhones have been simply the star of the present; iPhone gross sales got here in at $51.33B, up 1.5% Y/Y. Providers have been the quickest rising section, with income of $20.9B, up 5.4%. Apple additionally beat expectations on gross margins, reporting gross margins of 44.3% versus the consensus of 44.1%.

Nonetheless, total gross sales fell for the second consecutive quarter. We imagine the market is getting too excited too quickly about stronger iPhone gross sales as different product traces reported unfavourable progress. In 2Q23, Mac gross sales dropped 31% to $7.17B this quarter, iPad income declined 13% to $6.67B, and Wearables, House, and Equipment dropped barely by 1% to $8.7B. The next desk outlines Apple’s web gross sales by class:

Apple 2Q23 earnings outcomes.

We see restricted room for the corporate to develop within the close to time period apart from probably outperforming softer consensus expectations and don’t imagine that justifies shopping for Apple at present ranges. Apple’s one of many main customers of the semiconductor business; the corporate is Taiwan Semiconductor Manufacturing Firm Restricted’s (TSM) largest buyer. The semiconductor business is in oversupply, and stock correction cycles are underway on NAND and DRAM fronts. We anticipate stock digestion to help the smartphone and PC market restoration. Nonetheless, we see smartphone correction going down post-2Q23 incomes outcomes and see the inventory dropping additional in response.

Administration didn’t present clear steerage for the following quarter, which has been typical in previous quarters; what we do know is that CFO, Luca Maestri, stated on the earnings call:

“We anticipate our June quarter year-over-year income efficiency to be just like the March quarter assuming that the macroeconomic outlook doesn’t worsen.”

We advocate traders exit Apple inventory at present ranges on a brief alternative and revisit as soon as the draw back danger of correction has been factored into the inventory.

Valuation

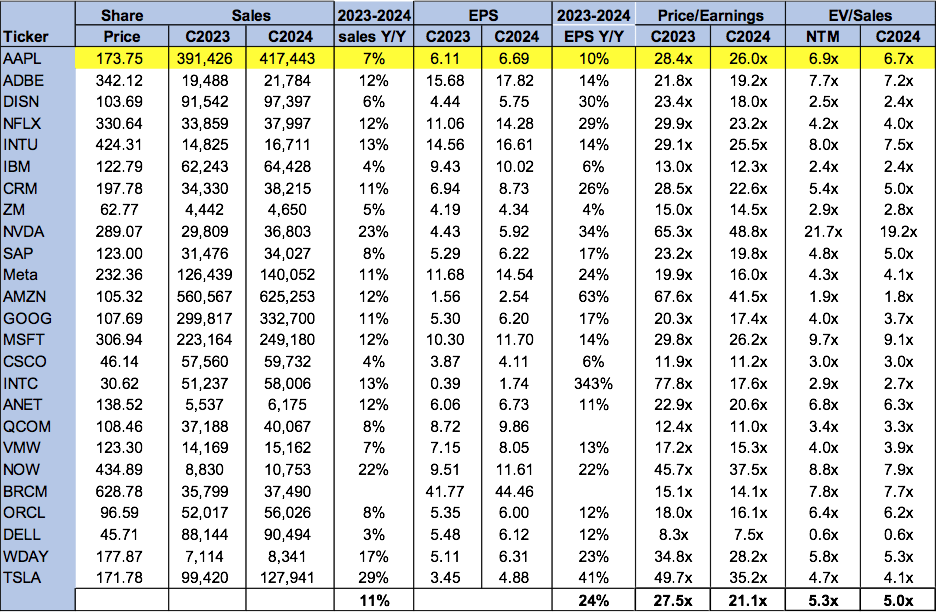

Apple Inc. isn’t low-cost, buying and selling at 26.0x C2024 EPS $6.69 on a P/E foundation in comparison with the peer group common of 21.1x. The inventory is buying and selling at 6.7x EV/C2024 gross sales versus the peer group common of 5.0x. We don’t see favorable entry factors into the inventory at present ranges; we see little room for upside within the close to time period and advocate traders promote the inventory at present ranges.

The next chart outlines Apple’s valuation in opposition to the peer group.

TechStockPros

Phrase on Wall Road

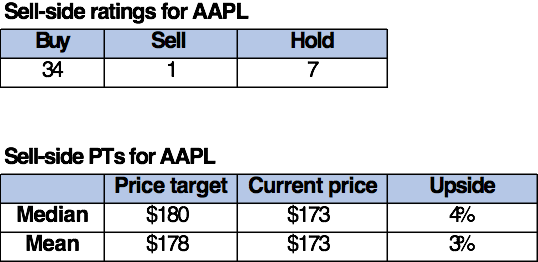

Wall Road is overwhelmingly bullish on the inventory. Of the 42 analysts protecting the inventory, 34 are buy-rated, seven are hold-rated, and the remaining are sell-rated. The bullish sentiment on the inventory is primarily pushed by Apple signaling indicators of restoration from the post-pandemic droop mixed with the better-than-expected 2Q23 incomes outcomes. Having stated that, Wall Road has been bullish on the inventory for a lot of the previous yr; we attribute this to Apple’s main standing inside smartphone markets and the corporate’s rising providers section. We’ll proceed to observe the inventory carefully to improve as soon as favorable entry factors seem.

The next chart outlines sell-side scores for Apple.

TechStockPros

What to do with Apple inventory

We’re downgrading Apple Inc. inventory to a promote, as we see favorable exit factors at present ranges. The corporate is recovering from post-pandemic weaker end-market demand on the iPhone entrance; nonetheless, we anticipate a correction in smartphone gross sales coupled with already declining Mac gross sales this quarter amid weakening PC demand.

We’re extra constructive on Apple than we’ve been for a lot of the previous yr, however simply don’t see favorable entry factors into the inventory at present ranges. We see additional draw back danger of correction and advocate traders exit Apple inventory at present ranges and revisit as soon as the chance has been factored in. We’ll proceed to observe the inventory to improve as soon as favorable entry factors materialize.

Our Investing Group, Tech Contrarians, might be launching on June 1st with a big low cost on the annual subscription for the lifetime of the service. We cowl the whole lot software program/{hardware} and semiconductors as engineers turned prime analysts. Hold studying our work to see extra of what’s forward.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.

[ad_2]