[ad_1]

IRINA NAZAROVA

Homebuilder M.D.C. Holdings, Inc. (NYSE:MDC) lately delivered optimistic steering that included energetic subdivisions’ depend on March 31, 2023 up by 18% y/y and new orders. Contemplating the optimism from administration and the present valuation, I imagine that designing a monetary mannequin is smart. In my view, profitable pricing methods, change within the mixture of dwelling choices, or extra initiatives in new areas might improve future FCF technology. Underneath my DCF mannequin, I imagine that the honest inventory value might be near $78 per share.

M.D.C. Holdings: A Lot Of Accrued Information And Optimistic 2023 Steering

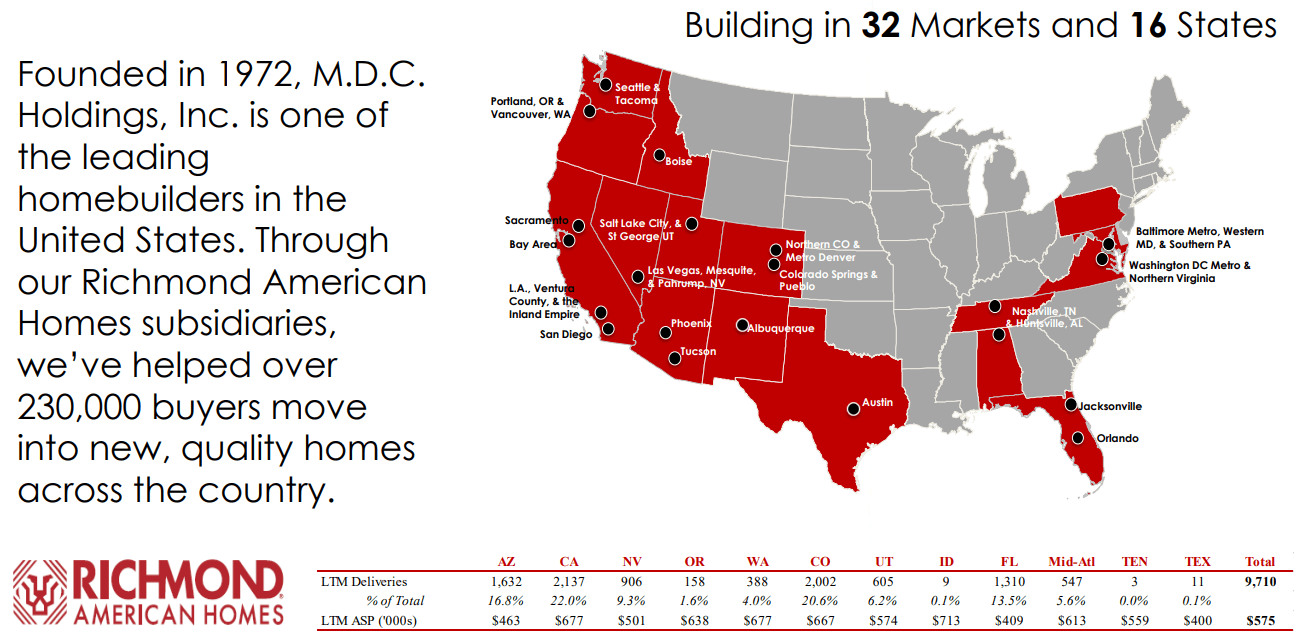

Homebuilder M.D.C. Holdings reviews experience collected from 1972 and a big checklist of dwelling deliveries everywhere in the nation. Contemplating the variety of financial crises that administration went by means of, I imagine that MDC is a should learn for real estate investors in the United States.

Supply: Investor Presentation

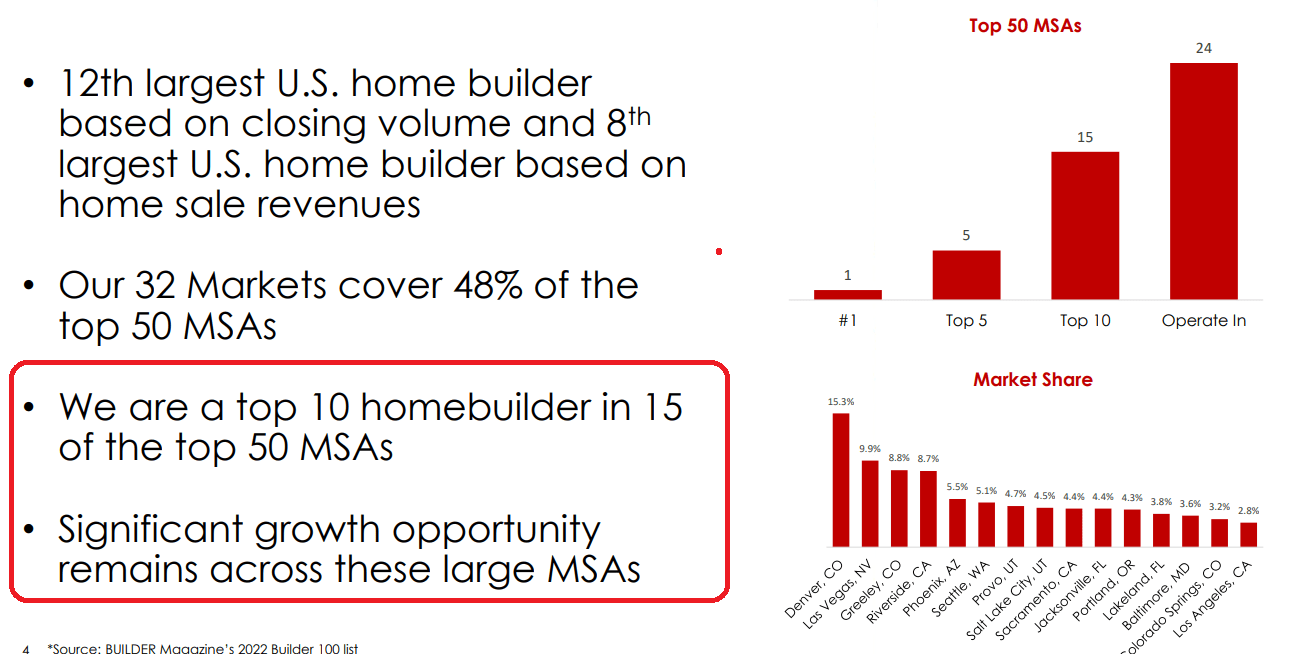

With that about what M.D.C. Holdings has completed and the truth that MDC seems to be the twelfth largest U.S. homebuilder within the US, it’s value noting that administration sees important progress alternatives throughout a number of metropolitan statistical areas. On this regard, the next slide was delivered in the newest quarterly report.

Supply: Investor Presentation

I’m fairly impressed by the current optimism exhibited within the most recent quarterly press release. Administration famous a major enhance within the variety of new orders within the first quarter as in comparison with that in This fall 2022. I additionally imagine that the expectations round future dividends will seemingly be appreciated by market contributors. For my part, if issues don’t go nice inside M.D.C. Holdings, dividends might decrease.

Because of a mixture of improved market circumstances and strategic pricing initiatives, now we have seen a rebound in homebuying exercise to start out the 12 months. Web new orders within the first quarter elevated considerably relative to the fourth quarter of 2022, as patrons returned to the marketplace for the beginning of the spring promoting season. Order momentum constructed because the quarter progressed, and we noticed order totals enhance on a sequential foundation every month. Supply: Press Launch

We imagine this places us in an excellent place to proceed our disciplined strategy to progress whereas concurrently funding our industry-leading dividend payout of $2.00 per share on an annualized foundation. Supply: Press Launch

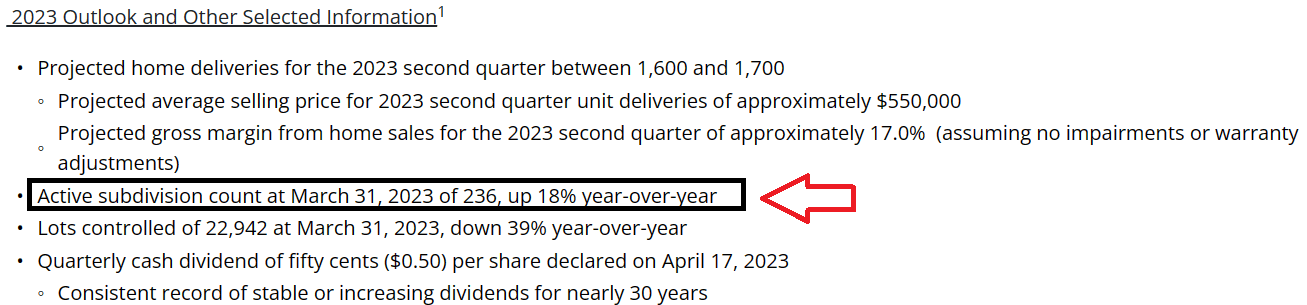

I additionally noticed that the steering given for 2023 was optimistic. Energetic subdivisions depend on March 31, 2023 was up by 18% y/y. In addition to, M.D.C. Holdings expects a projected gross margin dwelling gross sales of roughly 17%, so I don’t imagine that profitability can be a problem any time sooner or later.

Supply: Press Launch

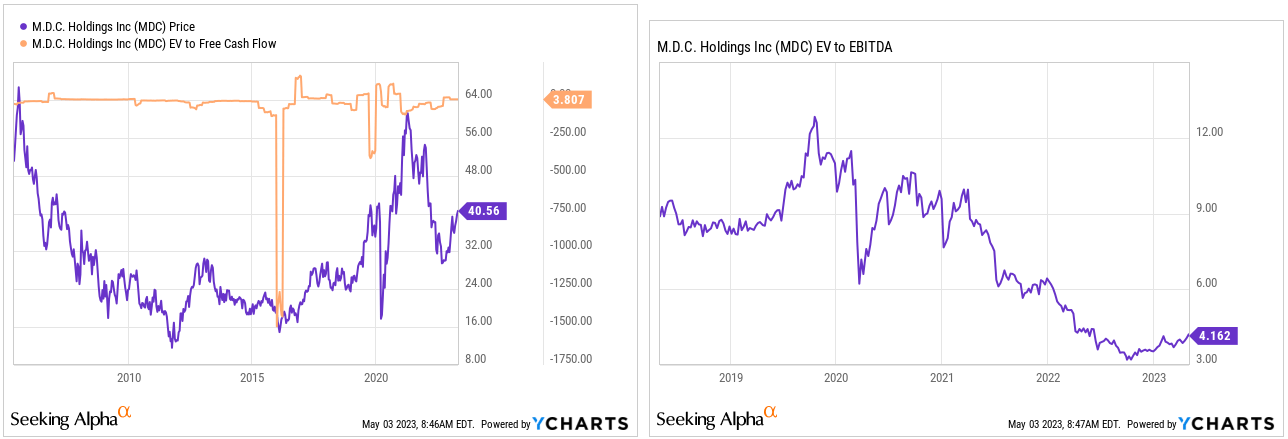

With the earlier details about numbers anticipated in 2023 and the present EV/EBITDA, which seems fairly low, I imagine that designing a cautious monetary mannequin about the future makes sense.

Supply: YCharts

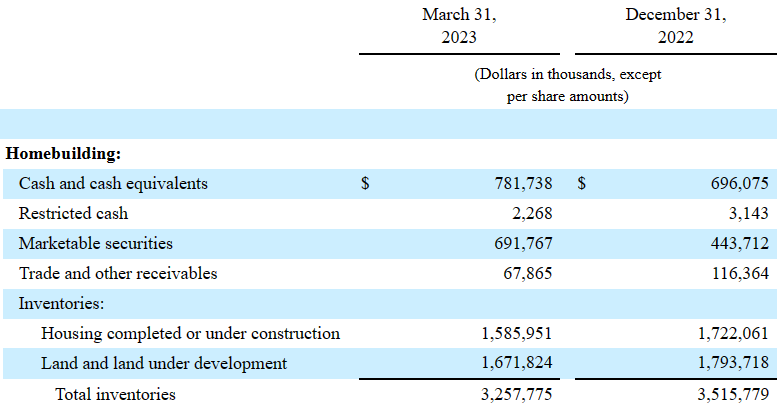

Property: Extra Money And Extra Whole Homebuilding Property

The steadiness sheet reported within the final 10-Q didn’t embrace a variety of adjustments as in comparison with that in This fall 2022. With that, it seems useful that administration reported a rise in money and marketable securities together with extra homebuilding property. I can not say that the enterprise is just not rising.

As of March 31, 2023, M.D.C. Holdings reported money and money equivalents of $781 million, restricted money of $2 million, and marketable securities value $691 million. Additionally, with commerce and different receivables of $67 million, housing accomplished or underneath development stands at $1.585 billion, with land and land underneath improvement of $1.671 billion, total inventories is equal to $3.257 billion.

Supply: 10-Q

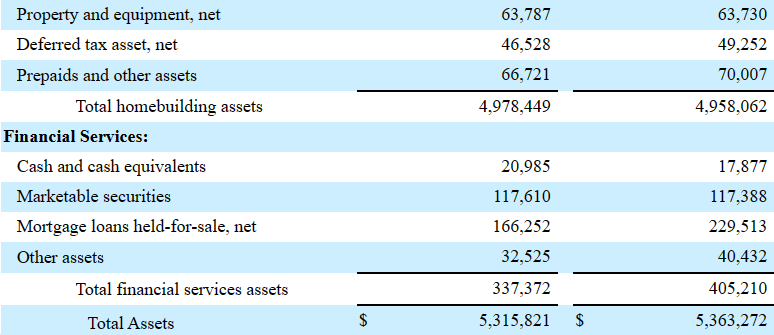

Property and gear stood at $63 million, with deferred tax property of $46 million and complete homebuilding property of $4.978 billion. With regard to monetary providers, the corporate reported money value $20 million, marketable securities round $117 million, and complete property near $5.315 billion. M.D.C. Holdings reviews an asset/legal responsibility ratio near 2x, so I feel that the steadiness sheet stands in a superb place.

Supply: 10-Q

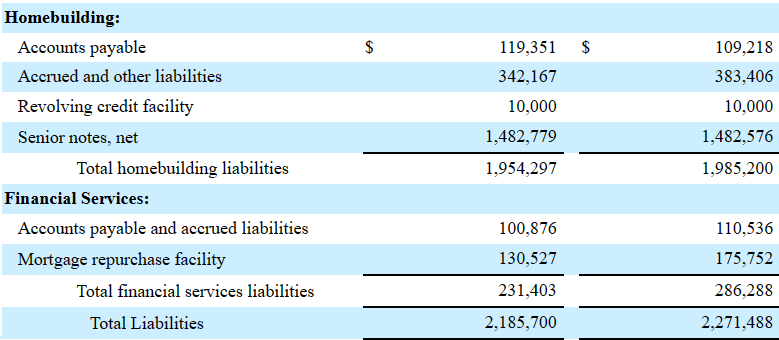

I Am Not Afraid Of The Whole Quantity Of Debt

The checklist of liabilities consists of accounts payable value $119 million, accrued and different liabilities of $342 million, a revolving credit score facility of $10 million, and senior notes of near $1.482 billion. I’m not involved in regards to the senior notes as a result of most of them mature around 2030-2061.

Supply: 10-k

Liabilities associated to monetary providers embrace accounts payable and accrued liabilities value $100 million, a mortgage repurchase facility value $130 million, and complete liabilities of $2.185 billion.

Supply: 10-Q

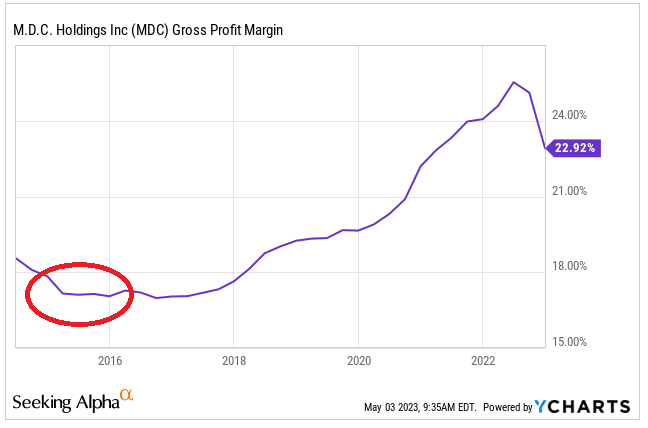

Pricing Methods, Change In The Combine Of Residence Choices, Or New Areas Might Suggest A Valuation Of $78 Per Share

Underneath my monetary mannequin for the following ten years, I assumed that administration will efficiently be capable to apply pricing methods as market circumstances change. In addition to, adjustments within the mixture of dwelling choices to cut back the prices of the homes might have a useful impact on the gross margins. Within the final ten years, administration knew nicely the best way to enhance the gross revenue margin, so I imagine that it is aware of the best way to do it sooner or later.

Supply: YCharts

I additionally imagine that MDC will efficiently handle to navigate potential provide chain obstacles. As well as, the collected experience coping with earlier provide chain points will seemingly assist.

Our groups did a superb job overcoming provide chain obstacles and municipal delays to shut houses in backlog in a well timed method. Supply: Press Launch

In addition to, I feel that additional growth into new territories might deliver a variety of income progress and maybe some economies of scale. On this regard, I might draw consideration to the variety of new openings in new areas.

Richmond American Properties of California, a subsidiary of M.D.C. Holdings, Inc. is worked up to announce the grand opening of Torrin at Valencia. Scheduled to open on Saturday, April 29, this dynamic new neighborhood boasts 4 impressed two- and three-story flooring plans with the open layouts and designer particulars immediately’s homebuyers are searching for. Supply: Richmond American Announces Grand Opening of New Valencia Community Richmond American Properties of Colorado, Inc., a subsidiary of M.D.C. Holdings, Inc., is happy to announce the grand opening of the ranch-style Cypress mannequin dwelling at North Vista Highlands in Pueblo. Richmond American Announces Grand Opening Event in Pueblo

Richmond American Properties of Tennessee, Inc., a subsidiary of M.D.C. Holdings, Inc., is worked up to announce the Grand Opening of Friendship Ridge in Hazel Inexperienced. Supply: Richmond American Announces Community Grand Opening in Hazel Green

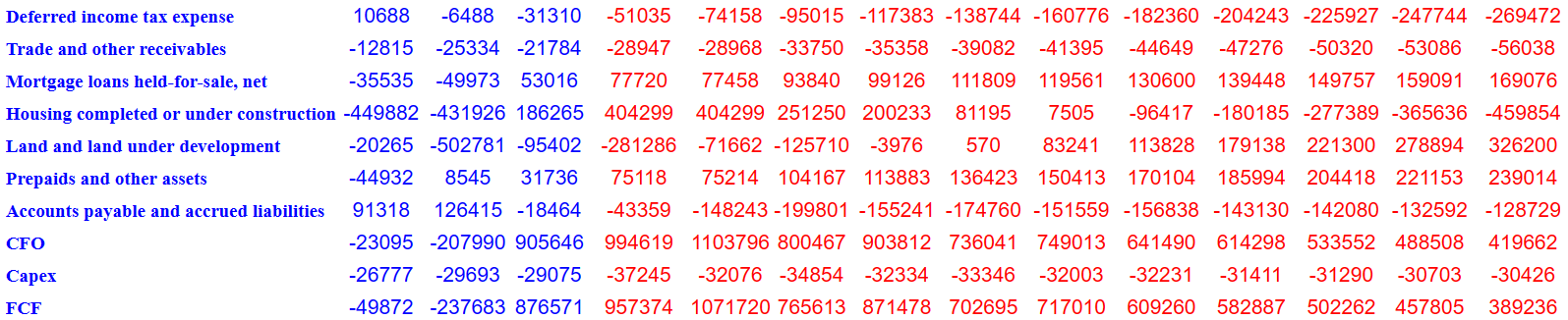

My DCF mannequin consists of 2033 internet revenue near $417.55 million, with stock-based compensation bills round $60.55 million, 2033 depreciation and amortization of $23.55 million, and 2033 venture abandonment prices of $98.55 million.

Supply: My DCF Mannequin

Up to now, the corporate included internet losses on marketable securities, features on sale of property, and amortization of debt securities for the calculation of the CFO. I do not imagine that these adjustments are crucial as they don’t symbolize every day actions of the enterprise mannequin reported by MDC.

Supply: My DCF Mannequin

I additionally included 2033 deferred revenue tax expense of -$270.55 million, commerce and different receivables of -57.5 million, mortgage loans held-for-sale near $169.5 million, and adjustments in housing accomplished or underneath development of -$460.5 million. In addition to, with land and land underneath improvement of $326.5 million, prepaids and different property near $239.5 million, and adjustments in accounts payable and accrued liabilities of -$129 million, 2033 CFO would stand at $419.5 million. Lastly, with capital expenditures of -$31.5 million, I obtained a 2033 FCF of $389.5 million.

Supply: My DCF Mannequin

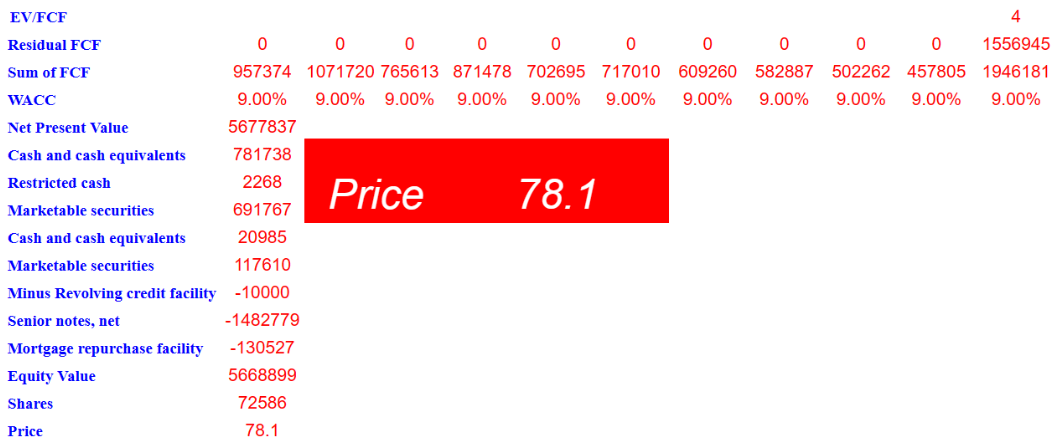

With a WACC of 9%, if we additionally assume a conservative EV/FCF ratio of 4x-5x, the web current worth of future free money circulation would stand at $5.67785 billion. I additionally added money and money equivalents of $781 million, restricted money of $2 million, marketable securities near $691 million, money and money equivalents from monetary providers of $20 million, and marketable securities from monetary providers of $117 million. In addition to, if we subtract a revolving credit score facility of -$10 million, senior notes value -$1.483 billion, and a mortgage repurchase facility of -$131 million, the fairness valuation would stand at $5.668 billion. Lastly, the implied honest value could be near $78 per share.

Supply: My DCF Mannequin

Danger Components

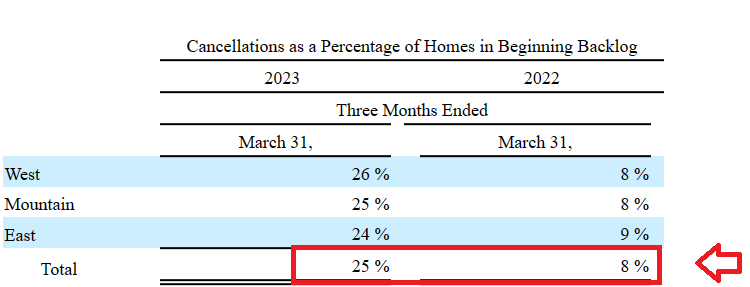

I’m a bit involved in regards to the enhance within the variety of cancellations reported within the quarter ended March 31, 2023. If cancellations proceed in Q2 and Q3, I imagine that the expectations for income progress would probably decline, which can push the inventory value even decrease.

Supply: 10-Q Supply: 10-k

M.D.C. Holdings reviews a considerable amount of housing accomplished or underneath development. If costs in the actual property {industry} decline, I imagine that most of the homes constructed could also be bought at a loss. MDC might have to cut back the valuation of those property within the steadiness sheet, which might deliver the e-book worth per share down. Because of this, many buyers would probably promote their shares, which can result in decrease demand for the inventory and inventory value declines.

If MDC fails to promote new homes, future free money circulation would probably decline, which can result in will increase within the internet leverage ratio. Because of this, market contributors could also be afraid of the entire quantity of debt, and may additionally resolve to promote their stakes within the MDC.

Lastly, labor circumstances, price of constructing supplies, or lack of those two crucial parts might considerably harm the money circulation assertion reported by MDC. In addition to, administration might not be capable to make predictions about future prices, which can result in decrease tasks and fewer houses obtainable.

We typically contract for our supplies and labor at a hard and fast value for the anticipated development interval of our houses. This permits us to mitigate the dangers related to will increase in the price of constructing supplies and labor between the time development begins on a house and the time it’s closed. Will increase in the price of constructing supplies and subcontracted labor might cut back gross margins from dwelling gross sales to the extent that market circumstances stop the restoration of elevated prices by means of larger dwelling gross sales costs. Sometimes and to various levels, we might expertise shortages within the availability of constructing supplies and/or labor in every of our markets. Supply: 10-k

Conclusion

M.D.C. Holdings reviews a major quantity of experience in constructing houses, and the newest steering given for the next quarter was useful. Contemplating the present financial surroundings, I’m fairly impressed by the optimism reported by administration. For my part, MDC inventory will seemingly ship profitable long run efficiency, so a long run monetary mannequin is smart right here. Profitable pricing methods, change within the mixture of dwelling choices, or the current initiatives in new areas will seemingly assist in providing working margin progress enhancements and FCF technology. Even considering potential dangers from volatility within the value of actual property property or difficult labor circumstances, I imagine that the inventory value might be value near $78 per share.

[ad_2]