[ad_1]

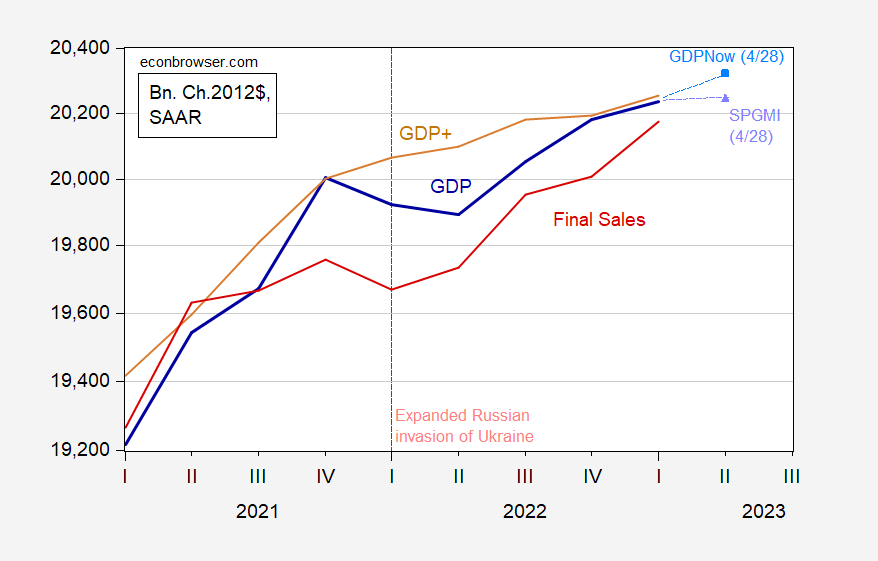

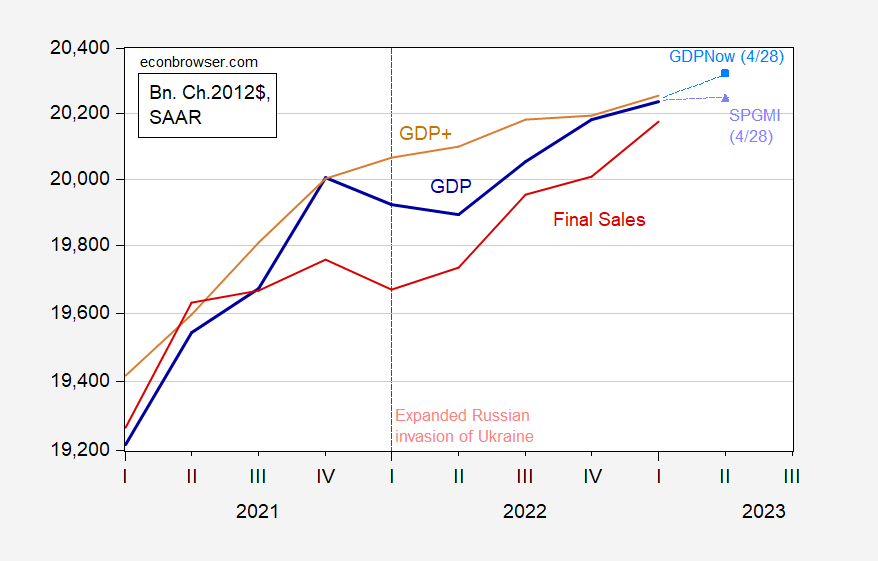

Jim famous recurrent delays within the lengthy heralded recession in his Thursday post. Listed here are some further reflections on the place financial exercise has been, and the place it’s heading, counting on further information. GDPNow (which hit the mark for Q1 development) signifies continued development via Q2. S&P International Market Insights (nee Macroeconomic Advisers) signifies a plateau has been reached. Last gross sales (i.e., GDP ex. inventories) suggests continued development.

Determine 1: GDP (daring darkish blue), GDP+ (tan), Last gross sales (crimson), GDPNow nowcast of 4/28 (sky blue sq.), S&PGMI monitoring as of 4/28 (lilac triangle), all in bn. Ch.2012$ SAAR. Supply: BEA 2023Q1 advance, Philadelphia Fed, Atlanta Fed, S&PGMI, and creator’s calculations.

My interpretation of those information, together with the truth that GDO and GDP+ appear to higher mirror the ultimately described trajectory of GDP (given the quite a few revisions that GDP receives over time), is that financial exercise decelerated (and combination demand really fell) in 2022H1, however no recession occurred, within the wake of the expanded Russian invasion of Ukraine and the following cost-push shock. Financial exercise is prone to proceed to rise into 2022Q2, though development will probably be anemic. As famous in a previous post, many forecasts peg a decline in 2022Q3 or 2022Q4.

[ad_2]