[ad_1]

MarsBars

It might have appeared like a good suggestion to purchase Treasury I Bonds final yr, when the yield was greater. Nevertheless, it’s essential to contemplate reinvestment threat, because the yield on I Bonds is now simply 4.3%, as a consequence of decrease inflation. Furthermore, buyers additionally quit alternative on the subject of high quality REITs (VNQ) which might be buying and selling at a reduction and pay a dependable and rising dividend.

This brings me to Camden Property Belief (NYSE:CPT), which I final lined here again in January, highlighting its sturdy working fundamentals. CPT stays materially down from the place it was 12 months in the past, having declined by 32%. On this article, I spotlight why CPT could also be a really perfect selection for worth buyers searching for doubtlessly sturdy revenue and complete returns, so let’s get began.

Why CPT?

Camden Property Belief is a self-managed, giant multifamily REIT that’s a member of the S&P 500 (SPY). It owns 172 properties at current overlaying 58K condo properties throughout the U.S., and is popular with workers, having been named as 100 Greatest Firms to Work for by Fortune journal for 16 consecutive years. The corporate is led by long-term CEO, Richard Campo, who has been with the corporate for 30+ years.

There’s a widespread perception that greater rates of interest are dangerous for REITs. That doesn’t seem like the case for top of the range REITs reminiscent of CPT within the multifamily phase. That’s as a result of greater mortgage charges lead to greater price of dwelling possession, thereby leading to stickier tenant relationships and better demand for well-located House REITs.

CPT seems to be one such REIT, because it noticed wholesome identical property NOI development of 8.1% YoY throughout the first quarter. This was pushed partly by wholesome demand for its properties, with a decent 4% blended lease unfold on signed new and renewal leases throughout the quarter. It seems that momentum accelerated considerably in April, because the blended lease unfold rose by 20 foundation factors to 4.2%. Whereas occupancy was down by 140 foundation factors YoY in April, it nonetheless stays at a stable 95.4%.

Close to time period headwinds embrace greater insurance coverage premiums this yr, which vary from 15% to twenty% improve, as insurance coverage suppliers are passing on greater prices associated to giant international losses. Nevertheless, administration plans to greater than offset greater working prices with hire will increase, with full yr steerage for five% identical retailer NOI development this yr.

Importantly, CPT is nicely ready to sort out potential headwinds, because it’s one of many few REITs on the market with an A- credit standing from S&P. That is mirrored by its sturdy steadiness sheet with a low internet debt to EBITDA ratio of 4.3x and $1.1 billion of liquidity. This offers CPT ample capability to fund its improvement pipeline, which is estimated to price $268 million over the following three years and add 6 extra properties, bringing complete properties to 178 by 2026.

Importantly, CPT pays a decent 3.6% yield, and the dividend has been uninterrupted for 13 years, and was not too long ago raised by 6.4%. It’s additionally well-protected by a 58% payout ratio, based mostly on Core FFO per share steerage of $6.86 for this full yr.

Lastly, CPT stays a great worth on the present value of $110 with a ahead P/FFO of 16.0, sitting comfortably beneath its regular P/FFO of 18.1. Analysts estimate between 4% and 6% annual FFO per share development by way of 2025, which may translate to ~9% annual complete returns over the following 3 years.

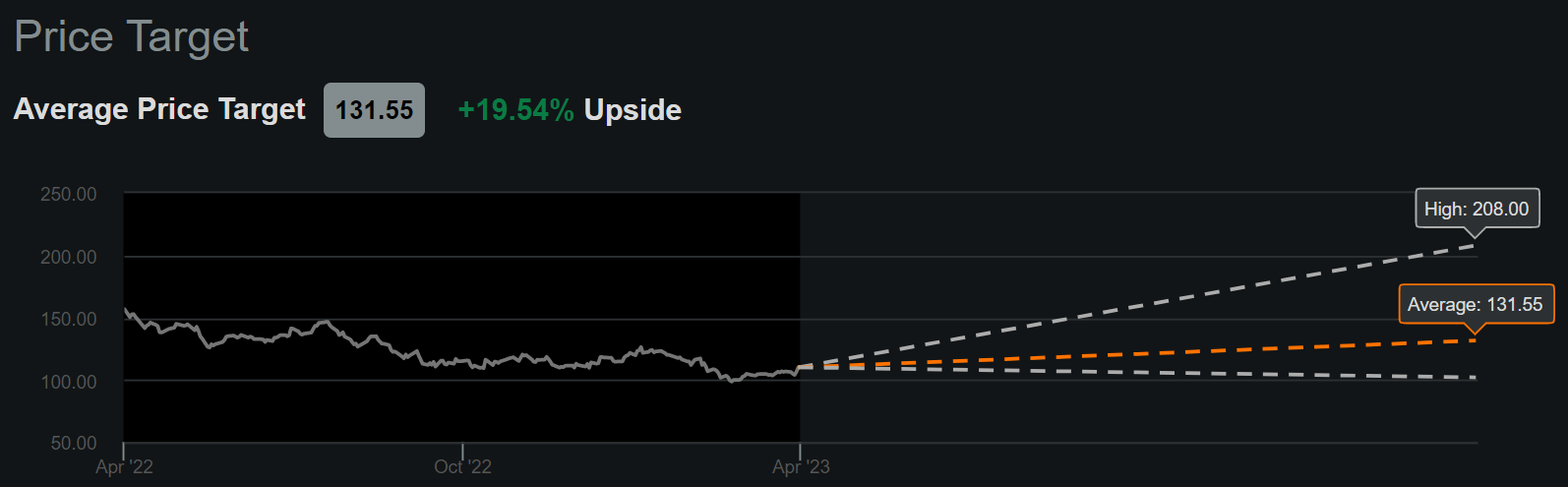

That is across the identical long-term return of the S&P 500, all whereas paying buyers a relatively far greater dividend yield. Promote aspect analysts who comply with the corporate have a consensus Purchase ranking with a median value goal of $131.55, which equates to a possible 23% complete return over the following 12 months.

Looking for Alpha

Investor Takeaway

Camden Property Belief is a high-quality House REIT that provides buyers a doubtlessly sturdy mixture of revenue and complete returns. The corporate has a robust steadiness sheet, and its dividend seems to be well-protected by a low payout ratio. It is also seeing wholesome lease spreads and administration is guiding for continued development this yr. Lastly, CPT may very well be an important possibility for individuals who prize revenue security and doubtlessly sturdy near-term returns if and when the market re-rates this premium REIT as a consequence of decrease inflation and rates of interest.

[ad_2]