[ad_1]

JHVEPhoto

Funding Thesis

Stryker Corp. (NYSE:SYK) is a medical gear know-how firm working in the USA and sells its merchandise internationally. It operates by two segments: Orthopedics and Backbone and MedSurg and Neurotechnology, which offer varied medical merchandise, together with implants, surgical navigation methods, and gear, amongst others. Its subsidiaries, branches, and third-party sellers promote its merchandise to healthcare amenities, docs, and hospitals.

The corporate is well-known for its high quality medical know-how within the medical sector. Its inventory surged in worth by 20.09% during the last twelve months. It’s with out shock contemplating its popularity for brand new modern merchandise and its resilience in opposition to international macroeconomic pressures. The corporate registered attractive prime and backside traces in 2022.

The stability sheet is very leveraged and has pretty excessive liquidity. Its working leverage can be excessive, with its fastened prices exceeding the variable prices. Moreover, SYK’s dividends have steadily grown, and funds have been made constantly. I am optimistic in regards to the firm’s efficiency and, due to this fact, bullish.

New Choices

Insignia Hip Stem

SYK not too long ago launched the Insignia Hip Stem, an implant designed to assist in optimizing affected person match and ease of implantation throughout complete hip procedures. This new addition enhances the corporate’s predominant hip portfolio. Its compatibility with Mako SmartRobotics enhances the procedures and the affected person end result.

Q Steerage System

This can be a navigation software program for backbone functions that the FDA has granted approval for utilization with pediatric sufferers 13 years previous and above. The navigation software program enhances computer-assisted surgical procedures by making preoperative planning, navigation, and execution less complicated.

These two are simply the tip of what Stryker affords, because it has an in depth portfolio. I discussed these since they contributed to revenues in 2022, albeit unclearly outlined, that are mentioned later.

Engaging however Anticipated Incomes

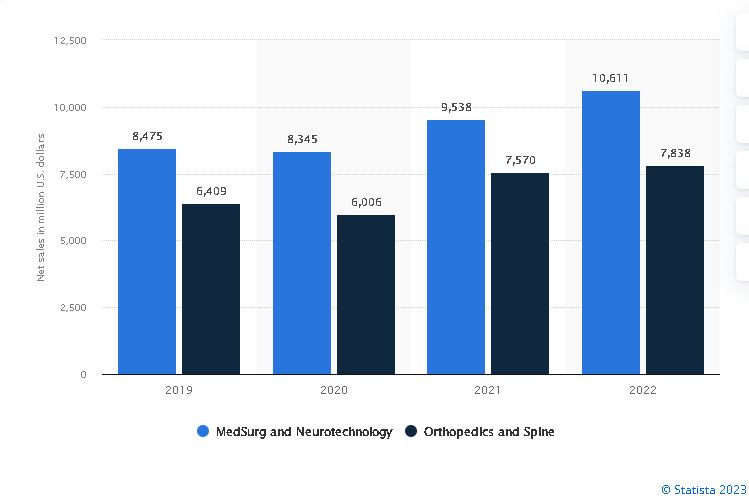

Stryker has skilled elevated revenues since 2019, besides in 2020 resulting from Covid19, which might be protected to say had it not been for the unprecedented well being disaster, revenues could be increased than in 2019. The corporate recorded engaging revenues throughout 2022, with its web gross sales at $18.4b, an 11% improve in fixed forex (cc). As talked about earlier, the corporate capabilities by two divisions, MedSurg and Neurotechnology, and Orthopedics and Backbone. MedSurg and Neurotechnology had web gross sales amounting to $10.6b, a 14.1% increment in cc from 2021, and natural web gross sales rising of 11.8% resulting from increased pricing and elevated gross sales quantity.

Statista

Orthopedics and Backbone had web gross sales at $7.8b, a rise of seven% from the earlier yr, and natural web gross sales surged 7%. The natural web gross sales improve on this section was additionally a results of increased gross sales quantity, which was partly offset by decrease pricing. In the latest quarter, the hip, trauma, and Backbone enterprise grew organically, partially contributed by the brand new Stryker choices. For instance: Hip enterprise grew 11.3%, pushed partly by the newly launched Insignia Hip Stem, suitable with Mako Complete Hip. Not too long ago accepted by the FDA, the freshly launched Q Steerage navigation system helped the Backbone enterprise develop barely by 0.5%.

The company reported a gross revenue margin of 63.1% TTM, a lower from the tip of 2021’s revenue margins at 65.8%. This may be traced to buying expensive elements and a worth surge alongside the provision chain. Nonetheless, its web revenue margin was 12.78%, a rise from 11.7%, and when evaluated in opposition to its friends, SYK carried out higher because the sector’s common gross revenue and web revenue margin have been 55.65% and -7.24%.

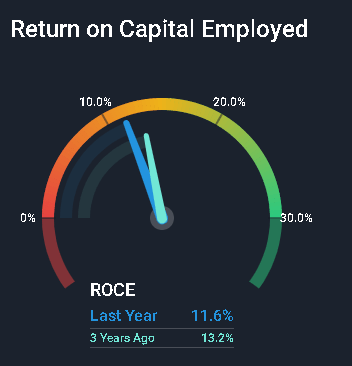

Stryker’s ROCE was 12%, which contrasted with the medical gear 9.9% trade carried out pretty effectively. That is additionally an enchancment from the prior years’ 11.6%.

Merely Wall Avenue

SYK, due to this fact, makes use of its capital effectively to generate earnings within the full yr 2022. On the flip facet, taking a look at its development, its ROCE has decreased from 14.5% over the previous 5 years. The development will not be very reassuring, and I urge buyers to intently monitor this.

Given the corporate’s broad portfolio of merchandise and its continued improvements, it’s set for a promising future. Contemplating its not too long ago launched choices chipped in its revenues, I’m optimistic that SYK will proceed with its unwavering progress in its revenues and earnings.

Financials

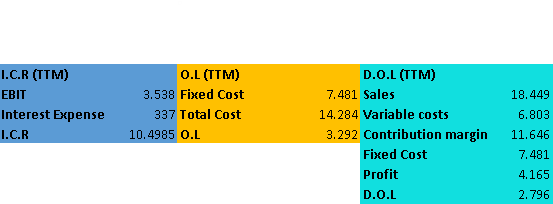

On this part, I shall dive into debt, its corresponding ratios, and its working leverage. The corporate has a debt of $13.526b and complete shareholders’ fairness of $16.616b. With these figures, the debt-to-equity ratio is 81.4%. It additionally has money accessible at $1.93b. Assuming Stryker pays its debt with this money stability, the web debt-to-equity ratio could be 69.7%. These ratios are significantly excessive, indicating that the corporate is very leveraged. Furthermore, during the last decade, the debt-to-equity ratio elevated from 72.4% in 2017 to 81.4%, signaling that debt will not be lowering.

It is very important consider debt and curiosity protection to know if the corporate can service its debt. The working money move at $2.62b is 22% of its debt, the principal quantity. This can be a constructive signal that the CFO effectively covers its debt. Curiosity bills arising from debt quantity to $337m. EBIT covers curiosity bills at $3.5b; due to this fact, the curiosity protection ratio is 10.5x. In gentle of this, SYK can cater to its debt arisen curiosity by roughly 10.5x.

The corporate has an working leverage (O.L) and diploma of working leverage of three.29 and a pair of.80. Which means that the working revenue is delicate to alter, and may its revenues improve, EBIT will even improve considerably and vice versa. Because the fastened prices are greater than the variable prices, this could possibly be one of many causes for the corporate’s skill to generate engaging margins.

Writer computations

Dividends

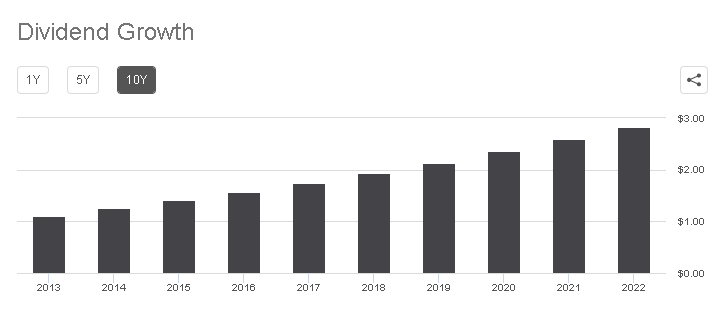

Stryker has upheld its picture concerning constantly paying dividends to its shareholders. It has consecutively paid dividends for 29 years in comparison with the 11-year common within the sector. The corporate additionally boasts rising dividends as its funds have elevated yearly over the previous ten years, suggesting that it’s financially steady and generates ample money flows to maintain and ramp up its dividend funds steadily.

Searching for Alpha

SYK has an affordable payout ratio of 46.84% and a money payout ratio of 51.62%, retaining important margins for reinvestment. In my opinion, these proportions are possible and sustainable. Recently, it elevated its quarterly dividend to $0.75 per share, a 7.9% improve from $0.695 per share within the earlier yr. I’ve confidence within the firm’s skill to maintain its dividend coverage and progress, given its modern path to progress that drives its success.

Conclusion

SYK makes a speciality of medical gear know-how and is famend for its modern merchandise. It has registered rising revenues within the MedSurg, Neurotechnology, Orthopedics, and Backbone segments. The corporate has alluring profitability ratios in comparison with its trade friends.

The stability sheet is very leveraged, although its excessive debt stage raises concern and ought to be monitored intently. It additionally has a excessive working leverage which may contribute to its constructive margins. Moreover, dividend funds have been made constantly and have grown over the previous years, reassuring buyers. On account of its excellence and consistency in dividend funds, I like to recommend SYK inventory to potential buyers on this trade.

[ad_2]