[ad_1]

All people’s ready for it, but it surely’s nonetheless not right here but.

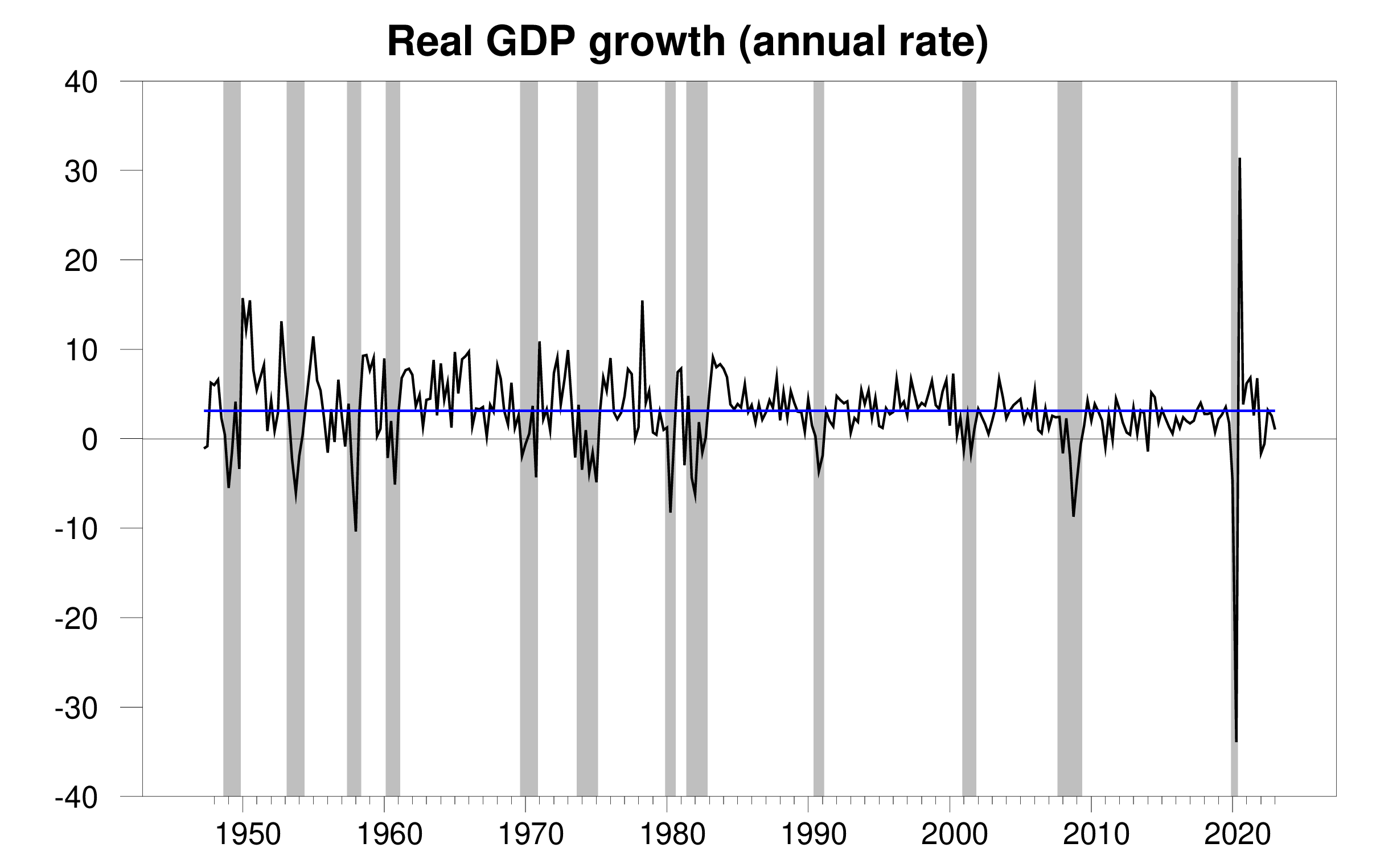

The Bureau of Economic Analysis introduced as we speak that seasonally adjusted U.S. actual GDP grew at a 1.1% annual charge within the first quarter. The earlier two quarters had been near the historic common. At the moment’s numbers are a lot weaker.

Actual GDP progress at an annual charge, 1947:Q2-2023:Q1, with the historic common (3.1%) in blue. Calculated as 400 instances the distinction within the pure log of GDP from the earlier quarter.

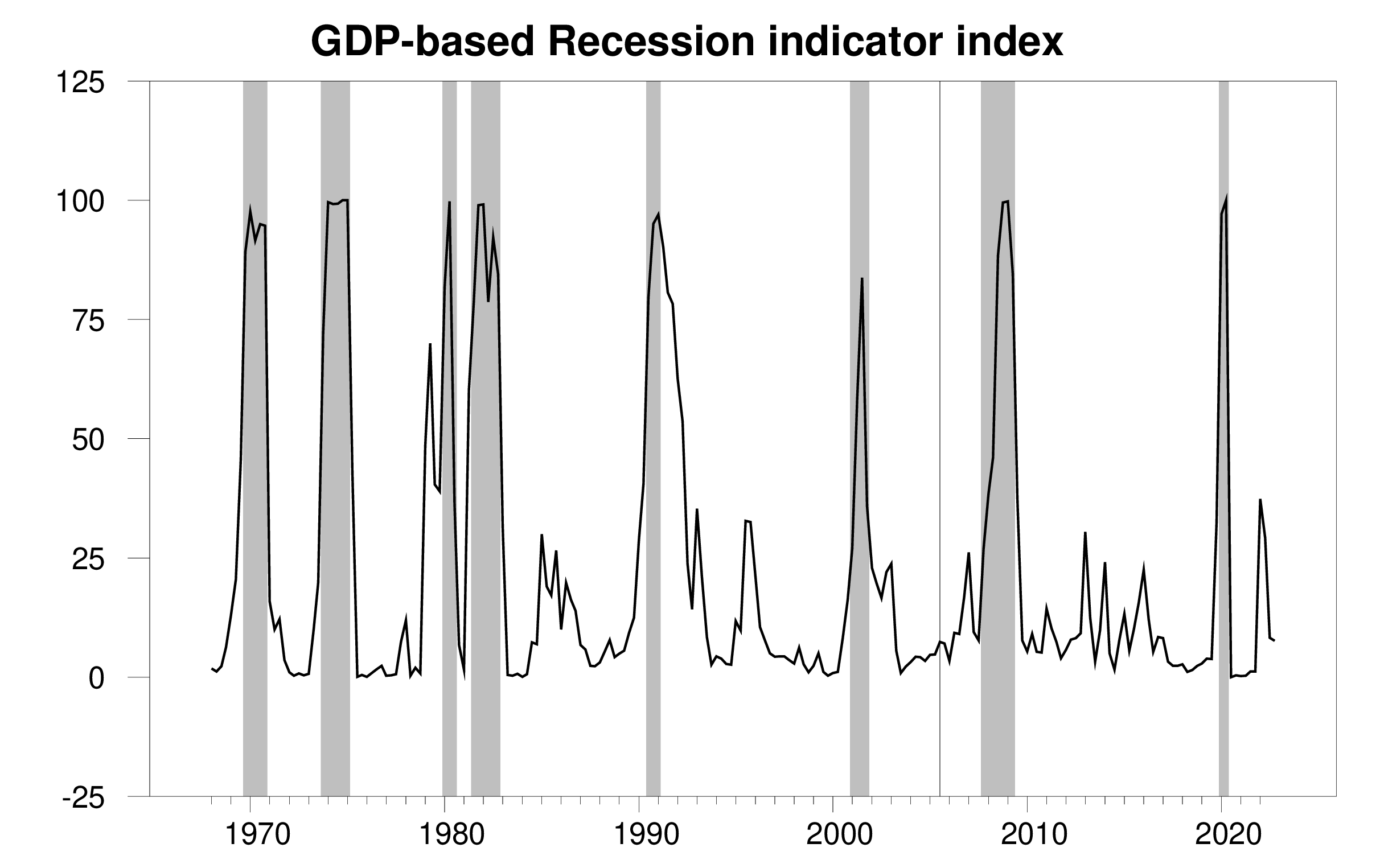

The brand new knowledge put the Econbrowser recession indicator index at 7.6%, about the place it had been three months in the past, and properly under the extent that will sign {that a} new recession had began. Those that have been declaring for a yr {that a} recession has already arrived should wait just a little longer.

GDP-based recession indicator index. The plotted worth for every date is predicated solely on the GDP numbers that have been publicly obtainable as of 1 quarter after the indicated date, with 2022:This fall the final date proven on the graph. Shaded areas signify the NBER’s dates for recessions, which dates weren’t utilized in any means in establishing the index.

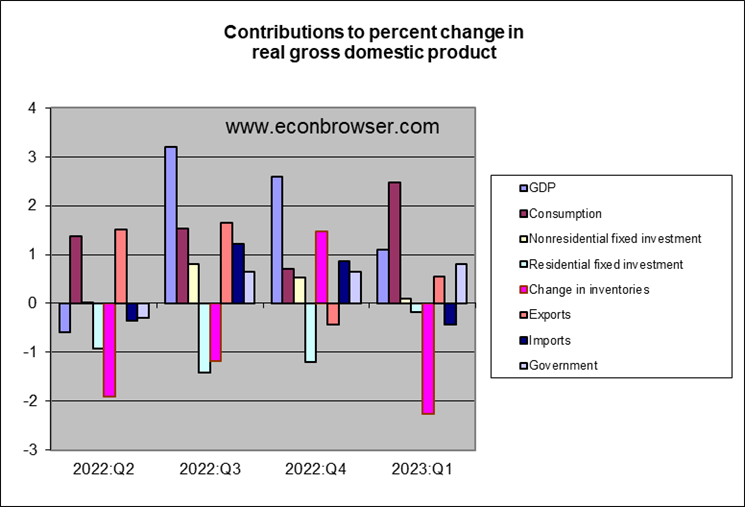

The Fed has been pushing the lever that it controls (rates of interest) within the route of making an attempt to sluggish GDP progress. This exhibits up first in residential fastened funding, which fell in every of the final 4 quarters.

However by far the most important drag on first-quarter GDP got here from operating down inventories. Stock funding is likely one of the most unstable elements of GDP and is topic to massive knowledge revisions. So that is unlikely to be the principle issue holding GDP progress again within the coming quarters. However the impact of excessive rates of interest on new residence purchases and spillover from banking considerations to credit score availability for small companies will proceed to be vital headwinds.

[ad_2]