[ad_1]

BING-JHEN HONG

April 6 proved to be something however a fantastic day for shareholders of Costco Wholesale (NASDAQ:COST). As of this writing, shares of the membership-based warehouse operator are down about 3.3% for the day after reporting, following the shut of the market on April 5, comparable retailer gross sales that disenchanted the funding group. Some traders could view this as a chance to purchase shares of the corporate on a budget. In spite of everything, Costco Wholesale is a high-quality firm that ought to proceed to develop in the long term. On the whole, I might agree that the market overreacted to the information that administration reported. However then again, experiencing draw back when even marginally unfavorable information is reported is the norm when shopping for shares of pricey companies.

Weak outcomes

On April 5, after the market closed, the administration staff at Costco Wholesale introduced comparable retailer gross sales information for the month of March, which is a five-week window ending April 2. Total income for the corporate got here in at $21.71 billion. That represents a rise of solely 0.5% in comparison with the $21.61 billion reported the identical window of time final 12 months. The composition of this lackluster gross sales enhance was pushed by combined outcomes from a geographical perspective.

Costco Wholesale

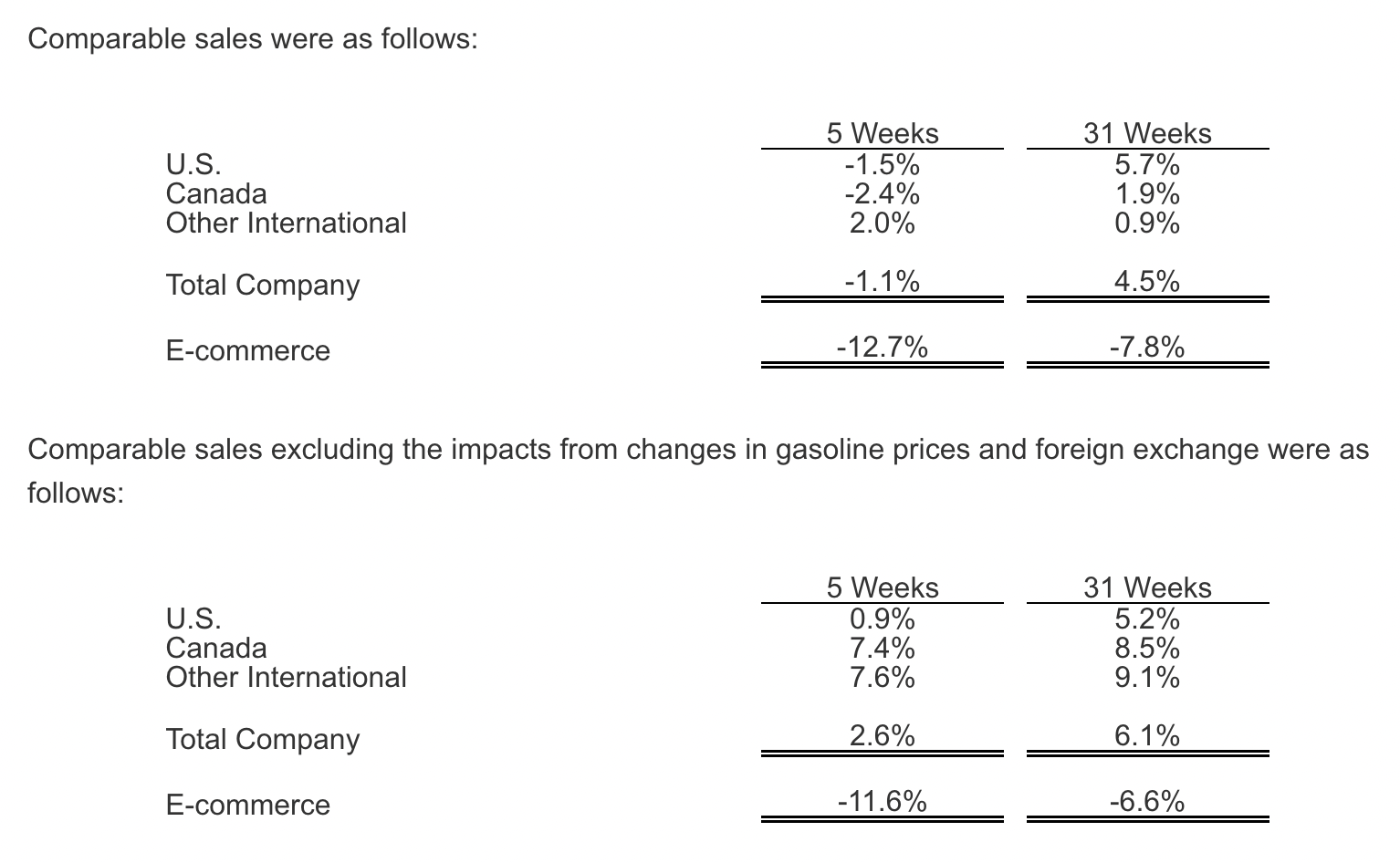

In the course of the five-week window in query, comparable gross sales reported by the corporate within the US managed to say no by 1.5%. Though for those who alter for modifications in gasoline costs and international forex fluctuations, this turns to a modest uptick of 0.9%. Canada noticed an analogous, however extra considerably pronounced, development. Comparable gross sales have been unfavorable to the tune of two.4%. However on an adjusted foundation, they turned optimistic by 7.4%. Different worldwide gross sales that exclude Canada reported a comparable gross sales enhance of two%. Although on an adjusted foundation, that determine strikes as much as 7.6%. All mixed, complete firm comparable gross sales dipped 1.1%, pushed by the numerous weighting that the US has on the corporate’s general monetary efficiency. However on an adjusted foundation, this quantity grew by 2.6%.

The largest weak point for the corporate throughout this time got here from its e-commerce operations. These truly dropped by 12.7%. And on an adjusted foundation, the image wasn’t higher, with a decline 12 months over 12 months of 11.6%. Whereas it is a drastic drop, it is necessary to notice that because the economic system reopened following the COVID-19 pandemic, extra individuals started going in-store versus ordering on-line. So some drop on this entrance was sure to occur.

Writer – SEC EDGAR Information

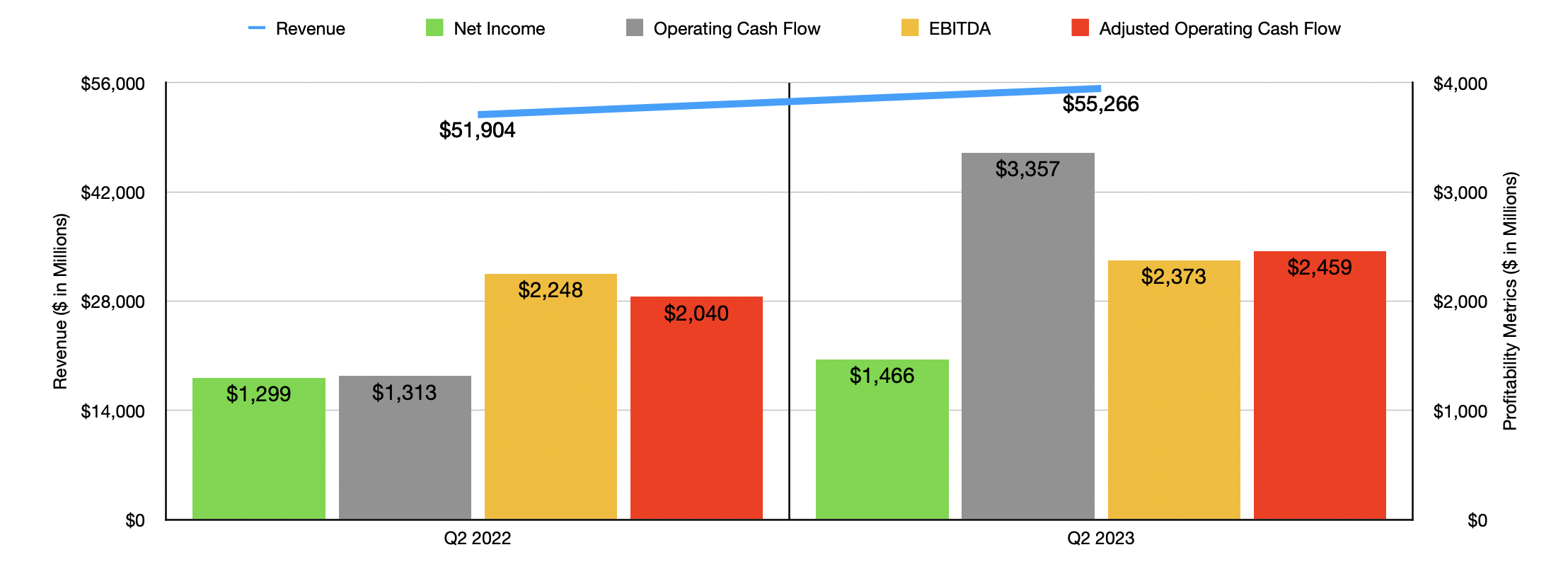

Except for the e-commerce information, these outcomes do not look horrible when positioned in a vacuum for an organization as massive and developed as Costco Wholesale occurs to be. However the motive why the market is disenchanted has to do with how briskly outcomes have weakened in comparison with earlier this 12 months. Again in January, I wrote an article protecting outcomes for the primary quarter of the corporate’s 2023 fiscal 12 months. Since then, administration has launched data protecting the second quarter of the 12 months as properly. Income for that point got here in at $55.27 billion. That represents a rise of 6.5% over the $51.90 billion reported just one 12 months earlier.

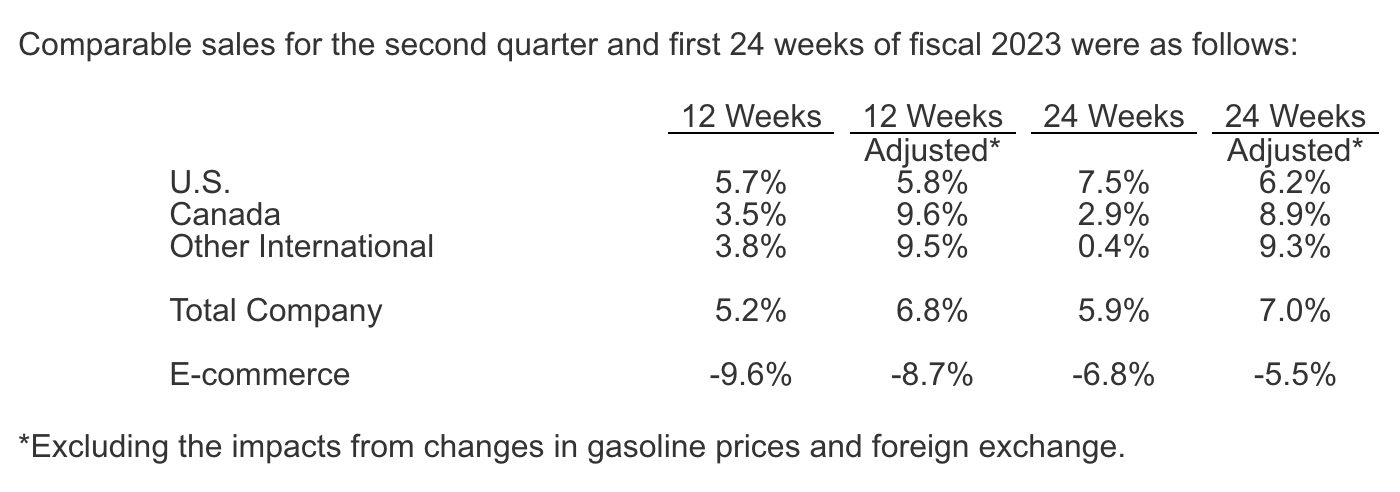

This upside was pushed largely by development in general firm comparable gross sales. This quantity was 5.2% greater than it was one 12 months earlier, with the adjusted determine coming in even stronger at 6.8%. At the moment, we did see weak point on the e-commerce facet, with gross sales down 9.6%, whereas the adjusted gross sales have been down 8.7%. However outdoors of that, outcomes have been pretty robust throughout the board. Probably the most placing distinction was within the U.S. market. Total income on a comparable gross sales foundation jumped by 5.7%, with an adjusted studying of 5.8%. And for the primary two quarters of the 2023 fiscal 12 months as an entire, the outcomes have been much more spectacular because the picture under illustrates.

Costco Wholesale

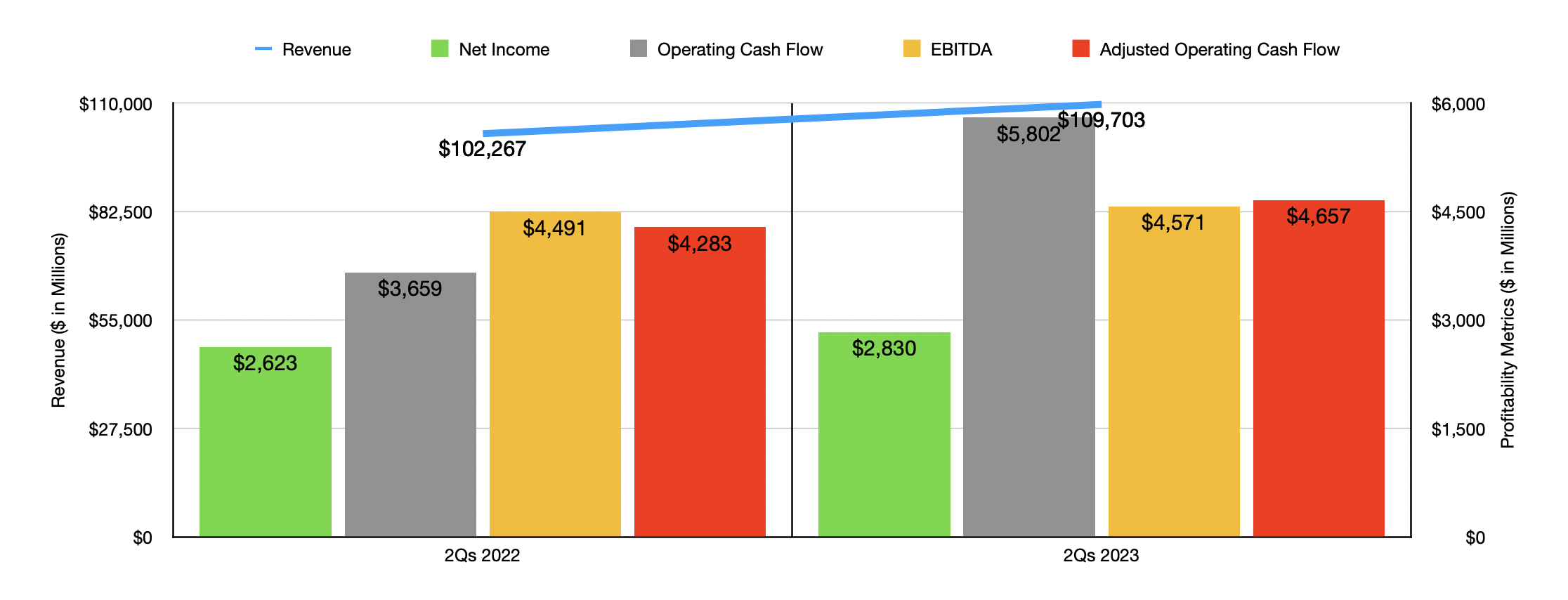

With the rise in income, the corporate additionally noticed development in its backside line outcomes. Web revenue totaled $1.47 billion. That is 12.9% above the $1.30 billion reported the identical time one 12 months earlier. Along with benefiting from a marginal enchancment in its gross revenue margin, the corporate additionally noticed curiosity revenue and different actions leap from $25 million to $114 million. An increase in rates of interest throughout the globe allowed the corporate to learn moderately considerably on this entrance. Whereas this will likely appear peculiar to some traders, think about that the corporate has money and money equivalents on its books of $13.71 billion. That compares to debt of $6.58 billion. With a lot money, even small enhancements within the rate of interest can have a optimistic affect on a agency’s backside line. Different profitability metrics adopted an analogous trajectory. Working money circulate, as an example, went from $1.31 billion to $3.36 billion. On an adjusted foundation, which makes changes for modifications in working capital, the metric would have gone from $2.04 billion to $2.46 billion. And eventually, EBITDA for the corporate expanded from $2.25 billion to $2.37 billion. As you’ll be able to see within the chart under, outcomes for the primary half of the 2023 fiscal 12 months as an entire got here in stronger than they did within the first half one 12 months earlier. Which means the outcomes skilled within the second quarter weren’t a one-time occasion.

Writer – SEC EDGAR Information

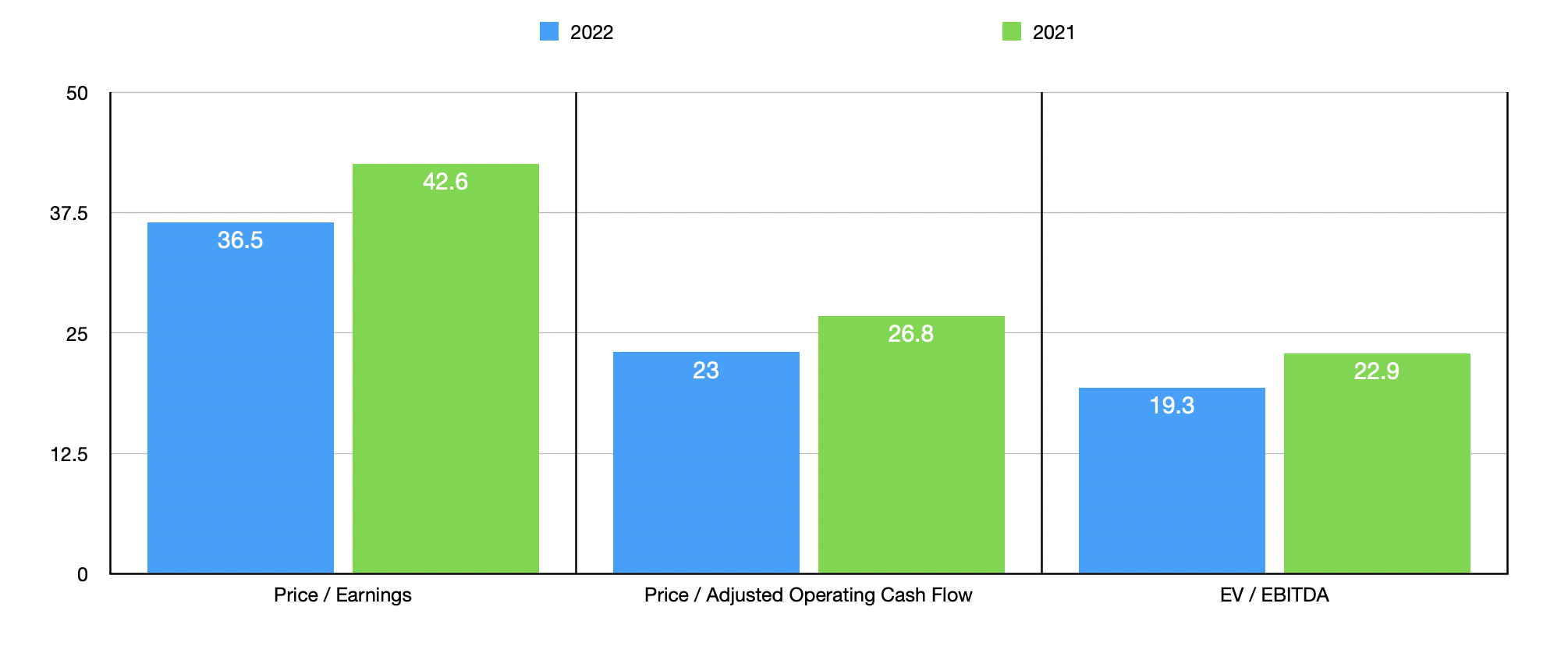

We do not actually know what the 2023 fiscal 12 months has in retailer for the corporate. Clearly, the image for the agency is weakening. Contemplating what is going on on within the broader economic system, this isn’t a shock and traders ought to count on it to proceed. Due to this, I didn’t forecast what sort of monetary efficiency the corporate would possibly expertise for 2023 in its entirety. But it surely’s protected to say that the primary half of the 12 months is just not a very good barometer of the place issues are going. I did, nonetheless, worth the corporate utilizing outcomes from each its 2021 and 2022 fiscal years. This information might be seen within the chart under.

Writer – SEC EDGAR Information

As you’ll be able to see right here, the corporate is at present buying and selling at a price-to-earnings a number of of 36.5. By itself, it is a very excessive a number of, particularly for such a big enterprise that ought to have restricted year-over-year development prospects shifting ahead. The worth to adjusted working money circulate a number of is significantly decrease, however nonetheless excessive, at 23. Aided by the surplus money that the corporate has on its books, the EV to EBITDA a number of of the agency is even decrease at 19.3. All of those numbers look higher than what the corporate reported for 2021. As you’ll be able to see within the desk under, I additionally in contrast Costco Wholesale to 5 related corporations. Utilizing all three valuation metrics, I discovered that it was the costliest of the group throughout the board.

| Firm | Worth / Earnings | Worth / Working Money Move | EV / EBITDA |

| Costco Wholesale | 36.5 | 23.0 | 19.3 |

| Walmart (WMT) | 35.0 | 14.2 | 14.7 |

| BJ’s Wholesale Membership Holdings (BJ) | 19.8 | 12.9 | 11.8 |

| Goal (TGT) | 27.3 | 18.9 | 13.6 |

| The Kroger Co. (KR) | 15.7 | 7.8 | 6.2 |

| Albertsons (ACI) | 8.7 | 4.1 | 3.2 |

Takeaway

In the long term, I’ve excessive hopes for Costco Wholesale from an operational perspective. It actually is a high-quality firm that ought to fare properly as time goes on. However this does not imply that the corporate is sensible to purchase into at this second. On an absolute foundation and relative to related corporations, shares of the retailer are extremely expensive. One might argue that the corporate warrants a premium due to its high quality. I might typically agree with this, which is why, up to now, I had rated it a ‘maintain’ as a substitute of a ‘promote’. I might additionally assert that the response to the weak comparable retailer gross sales was an overreaction and short-sighted within the grand scheme of issues. However between this weakening and the way expensive shares stay, I consider {that a} ‘maintain’ ranking remains to be applicable presently.

[ad_2]