[ad_1]

Kobus Louw

Westwood Holdings Group (NYSE:WHG) is an funding supervisor with $14 billion in AUM.

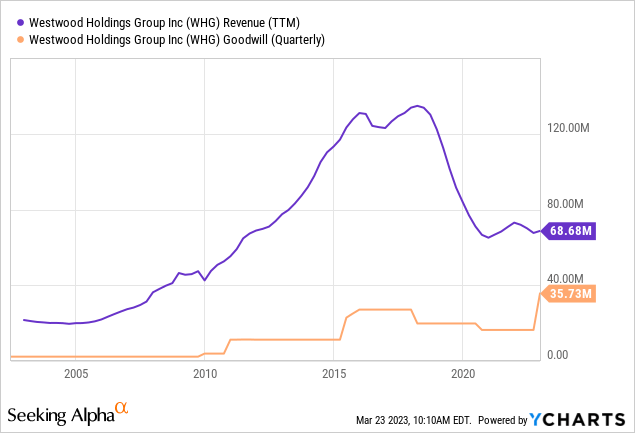

The corporate’s merchandise consist largely of mutual funds and energetic methods provided to establishments and high-net-worth people. Energetic cash managers have suffered web outflows for many years, and WHG isn’t any completely different, with natural web outflows in 11 out of the previous 15 years (and 9 of the previous 9).

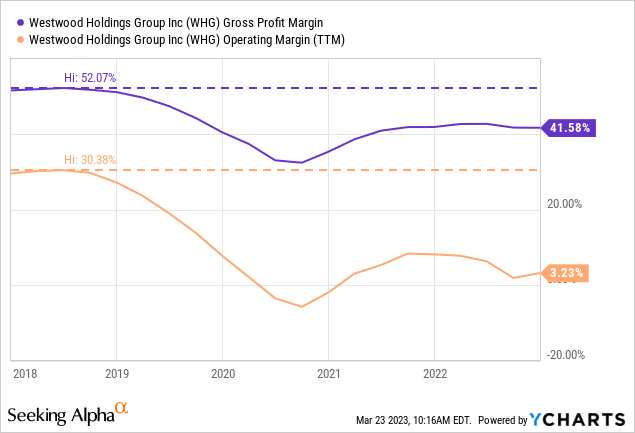

Including to the issue, WHG has been unable to regulate its value construction, largely composed of worker compensation, to guard profitability. The corporate’s prices have been diminished, however nonetheless, the corporate’s margins have collapsed.

WHG’s long-term headwinds will not be anticipated to vanish, and the corporate has been unable to adapt. WHG’s dividends are poorly coated, and most share buybacks are re-issued as share-based compensation.

The corporate is just not a possibility at these costs.

Observe: Except in any other case acknowledged, all data has been obtained from WHG’s filings with the SEC.

Enterprise description

Trade headwinds: As talked about in my article about Hennessy Advisors (HNNA), the energetic public funding administration trade has been severely broken by the proliferation of passive automobiles.

These automobiles don’t cowl solely easy methods like lengthy the S&P 500 or brief Treasury bonds. They permit establishments and retail traders to allocate extra advanced mixtures, selecting sectors, market caps, geographies, types, and so on. Additional, at a fraction of the associated fee and considerably comparable returns because the mutual fund or energetic technique counterparts.

WHG has not been resistant to this development, with natural web outflows in 11 out of the previous 15 years and yearly since 2014. The corporate has counteracted this by buying different funds, however the natural development is simply too robust.

Self-inflicted wounds: The income fall is a actuality, though the corporate may have perceived that development earlier and moved in direction of extra protected realms (like actual property or non-public fairness), solely doing so in 2022 with the acquisition of Salient Companions.

Nonetheless, the corporate may have diminished its workforce or the compensation that it pays to that workforce to guard profitability. I perceive that is simpler stated than achieved as a result of funding managers usually have vital operational leverage (on the upside and the draw back).

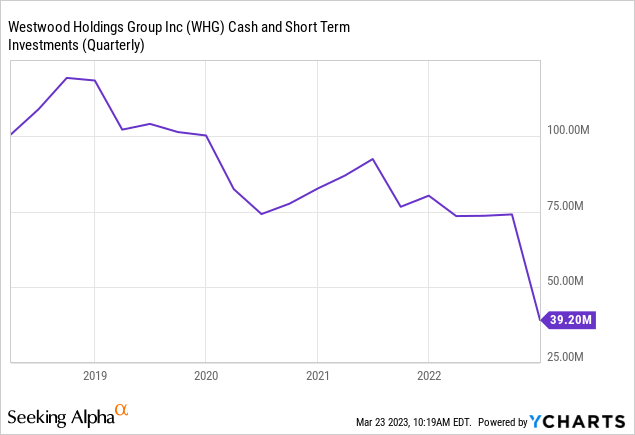

Robust stability sheet: The corporate amassed vital money and funding reserves when it was a really worthwhile (30% working margin) enterprise. A part of these reserves remains to be with the corporate.

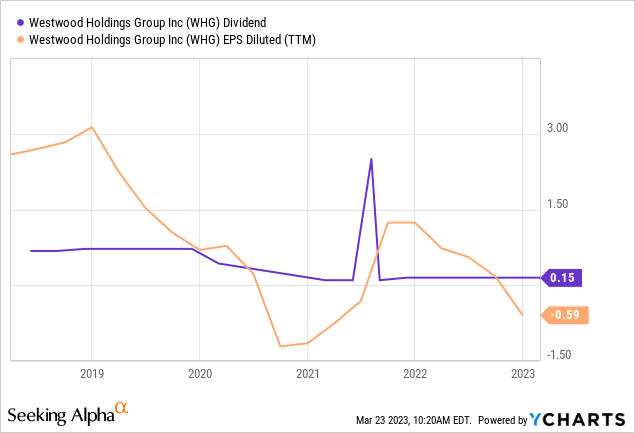

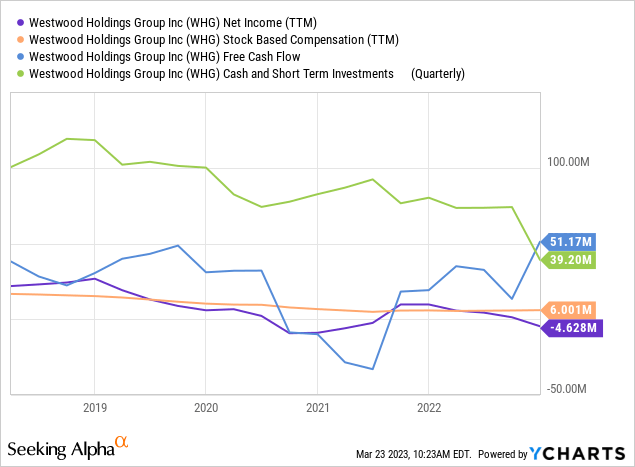

Paying dividends out of capital: The corporate has paid extraordinary dividends to shareholders that aren’t coated by earnings and subsequently are a return of capital. These dividends shouldn’t be thought of recurrent. As of FY22, the corporate is just not overlaying its dividend with working earnings.

Money flows are not any higher: The corporate boasts significantly better FCF than web revenue. Nevertheless, the distinction is usually defined by stock-based compensation and the incorporation of modifications in securities as a part of the CFO (often goes in money from investing).

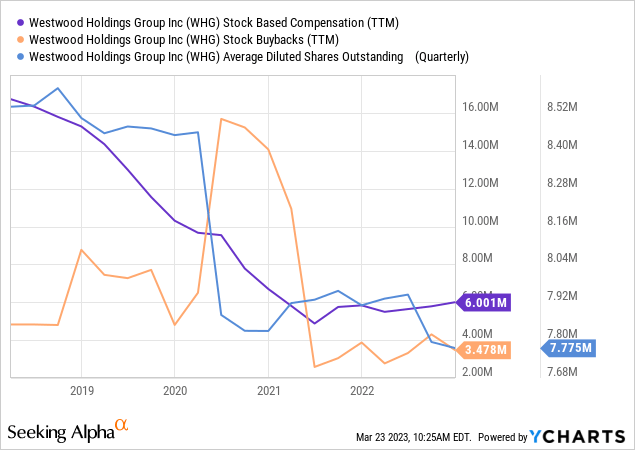

Additional, the corporate’s share repurchases are solely helpful to cowl the stock-based compensation, with the general share rely remaining stagnant. Even the massive buy of 2020 solely decreased the share rely by 8%.

Valuation

Shifting to options: The declining public enterprise is a actuality. The corporate has now entered the realm of other investments and actual property by buying Salient Companions, with an AUM of $2.7 billion, for $33 million.

Salient has choices in non-public fairness, actual property like wind farms, and a commodities buying and selling arm. This variation is wholesome, on condition that the headwinds in opposition to energetic managers haven’t disappeared, however doesn’t assure profitability development.

The choice investments trade can also be aggressive and will have grown quick solely beneath the safety of QE and low charges for the previous 15 years. For instance, Salient managed $27 billion as shut as 2015 however was bought whereas managing solely $2.7 billion.

Multiples: WHG generated web losses in 2020 and 2022, partly fueled by losses on their investments and the sale of their European subsidiaries.

However additionally they generated working losses in these two years. Suppose we take away acquisition prices from the Salient deal ($7 million over a $33 million deal, excessive) and impairment bills in 2020 ($3.5 million). In that case, we arrive at $1 million in working revenue for 2020, $6 million for 2021, and $2 million for 2022.

The common of $3 million may very well be thought of a measure of profitability. After all, ignoring the bills we now have not added and the funding losses.

Westwood trades at a market cap of $95 million, or a 32x a number of of adjusted common working revenue. For an organization struggling constantly from robust trade headwinds, it appears extreme.

After all, WHG’s mounted value construction can considerably enhance working revenue by a comparatively small enhance in income. The issue, in my view, is that development ought to be substantial to return even a ten% earnings yield (contemplating taxes, which we keep away from when utilizing the a number of on working revenue) and that these earnings ought to be sustainable, which isn’t assured given the trade backdrop.

Conclusions

WHG has suffered from its trade’s ailment, unable to develop organically for a lot of the previous 15 years.

The corporate grew by acquisitions however couldn’t act in opposition to the larger development and transfer earlier into options. Final 12 months’s acquisition of Salient might not be sufficient to revitalize the corporate, significantly if the choice funding trade suffers from excessive rates of interest.

The issue is just not the context or the corporate however the inventory’s value. At present costs, the corporate trades at an unlimited a number of of adjusted working income.

That value incorporates a major enchancment in profitability (at the very least quadrupling working income or rising revenues by 10% given the working leverage), but in addition sustainability on these income, one thing that the context doesn’t assure in any respect.

Due to this fact, I imagine WHG is just not a possibility at these costs.

Editor’s Observe: This text covers a number of microcap shares. Please concentrate on the dangers related to these shares.

[ad_2]