[ad_1]

APCortizasJr

Earnings of Cambridge Bancorp (NASDAQ:CATC) will seemingly enhance this yr on the again of a lagged impact of final yr’s charge hikes on the web curiosity margin. Additional, subdued mortgage progress will assist the underside line. General, I am anticipating Cambridge Bancorp to report earnings of $8.29 per share for 2023, up 14% year-over-year. In comparison with my last report on the corporate, I’ve solely barely decreased my earnings estimate for this yr. The year-end goal worth suggests a excessive upside from the present market worth. Subsequently, I’m sustaining a purchase ranking on Cambridge Bancorp.

Mortgage Progress Prone to Drop to Low-to-Mid-Single-Digit Vary

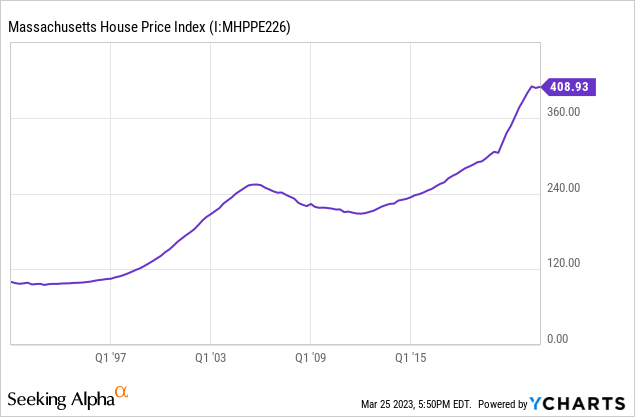

The mortgage portfolio grew by 12% within the fourth quarter because of the acquisition of Northmark Financial institution in addition to robust natural progress. Mortgage progress will decelerate this yr as borrowing prices are a lot increased now. Residential mortgage loans are extremely depending on mortgage charges; subsequently, this section will seemingly stay lackluster in 2023. Residential loans make up 41% of complete loans; therefore, the slowdown on this section can have a big impact on the whole mortgage progress. On the plus facet, the home worth index for Massachusetts has flattened just lately, which is nice information for housing affordability in Cambridge Bancorp’s primary market.

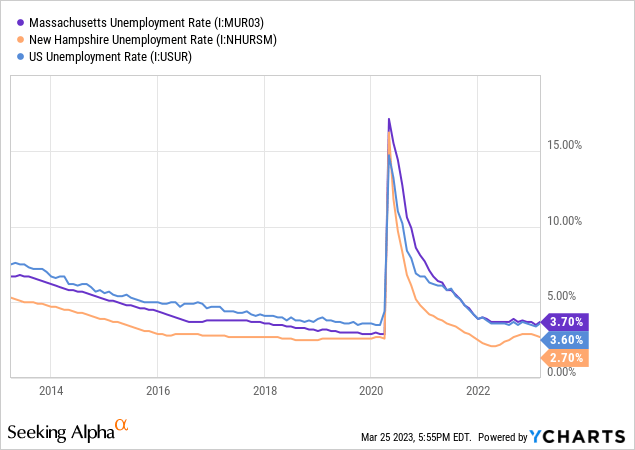

Additional, the outlook for industrial loans stays optimistic because the unemployment charge is persistently at a low degree. Cambridge Bancorp principally operates in Massachusetts with some presence in New Hampshire. As seen under, each states at the moment have very low unemployment charges when in comparison with their respective histories.

The administration talked about within the conference call that it’s anticipating mortgage progress to be between 0% to five% this yr. Contemplating the elements given above and administration’s steering, I am anticipating the mortgage portfolio to develop by 4% in 2023. The next desk exhibits my stability sheet estimates.

| Monetary Place | FY18 | FY19 | FY20 | FY21 | FY22 | FY23E |

| Web Loans | 1,543 | 2,209 | 3,118 | 3,285 | 4,025 | 4,189 |

| Progress of Web Loans | 15.5% | 43.1% | 41.2% | 5.4% | 22.5% | 4.1% |

| Different Incomes Property | 451 | 400 | 492 | 1,176 | 1,205 | 1,242 |

| Deposits | 1,811 | 2,359 | 3,403 | 4,331 | 4,815 | 5,011 |

| Borrowings and Sub-Debt | 93 | 136 | 33 | 17 | 133 | 137 |

| Frequent fairness | 167 | 287 | 402 | 438 | 518 | 561 |

| Ebook Worth Per Share ($) | 40.8 | 61.5 | 63.3 | 62.6 | 66.2 | 71.8 |

| Tangible BVPS ($) | 40.7 | 54.1 | 54.7 | 54.8 | 57.0 | 62.6 |

| Supply: SEC Filings, Creator’s Estimates(In USD million except in any other case specified) | ||||||

Margin to Fare Higher in 2023

Cambridge Bancorp’s internet curiosity margin grew by 13 foundation factors within the fourth quarter of 2022, which is not unhealthy contemplating the stability sheet positioning. The corporate’s loans and deposits are positioned in such a way that deposit re-pricing and mortgage re-pricing nearly cancel one another out within the first yr of charge hikes. Nonetheless, within the second yr, mortgage re-pricing can overtake deposit re-pricing. The outcomes of the administration’s rate-sensitivity evaluation given within the 10-K filing present {that a} 200-basis factors hike in rates of interest can enhance the web curiosity earnings by simply 0.4% within the first yr after which by 12.8% within the second yr of the speed hike.

As the primary charge hike within the present up-rate cycle was on March 16, 2022, we’re now within the second yr of the cycle. Subsequently, from the second quarter of 2023 onwards we will anticipate to see the margin considerably profit from final March’s charge hike.

Contemplating these elements, I am anticipating the margin to develop by 25 foundation factors in 2023, after falling by 20 foundation factors in 2022.

Anticipating Earnings to Develop by 14%

The anticipated margin growth and mortgage progress mentioned above will drive earnings this yr. Then again, inflation-driven progress of working bills will limit the underside line’s progress. General, I am anticipating Cambridge Bancorp to report earnings of $8.29 per share for 2023, up 14% year-over-year. The next desk exhibits my earnings assertion estimates.

| Revenue Assertion | FY18 | FY19 | FY20 | FY21 | FY22 | FY23E |

| Web curiosity earnings | 64 | 79 | 120 | 128 | 143 | 179 |

| Provision for mortgage losses | 2 | 3 | 18 | (1) | 4 | 4 |

| Non-interest earnings | 33 | 36 | 40 | 44 | 43 | 41 |

| Non-interest expense | 64 | 78 | 98 | 100 | 110 | 127 |

| Web earnings – Frequent Sh. | 24 | 25 | 32 | 54 | 53 | 65 |

| EPS – Diluted ($) | 5.77 | 5.37 | 5.03 | 7.69 | 7.30 | 8.29 |

| Supply: SEC Filings, Earnings Releases, Creator’s Estimates(In USD million except in any other case specified) | ||||||

In my final report on Cambridge Bancorp, I estimated earnings of $8.49 per share for 2023. I’ve tweaked nearly all line objects following the fourth quarter’s outcomes, which had been principally in step with my expectations. As I have not made any huge adjustments, my up to date estimate is near my earlier estimate.

Dangers Seem Comparatively Low

Cambridge Bancorp’s danger degree seems low regardless of the continuing banking sector disaster because of the following causes.

- The gross unrealized loss on the available-for-sale securities portfolio was solely $28.6 million on the finish of December 2022, as talked about within the 10-Okay submitting. To place this quantity in perspective, $28.6 million is simply 6% of the fairness excellent on the finish of final yr and round half of the web earnings reported for 2022. In case there’s a deposit run à la SVB Monetary Group’s (SIVB) case, and Cambridge sells its securities portfolio, then the unrealized losses will flip into realized losses. Nonetheless, this excessive case would not fear me as a result of the hit might be solely half of earnings and simply 6% of fairness.

- Cambridge would not have publicity to dangerous asset courses, together with crypto belongings, digital tokens, or enterprise capital, not like the U.S. banks which have failed to this point (Signature Financial institution (SBNY), Silvergate Capital (SI), and SVB Monetary Group).

- The corporate seems extra than simply well-capitalized. It reported a complete capital ratio of 13.52% for the top of December 2022, which is way increased than the minimal regulatory requirement of 10.50%.

Excessive Complete Anticipated Return Justifies a Purchase Score

Cambridge Bancorp is providing a dividend yield of 4.0% on the present quarterly dividend charge of $0.67 per share. The earnings and dividend estimates recommend a payout ratio of 32% for 2023, which is under the five-year common of 39%. Subsequently, the dividend seems safe.

I’m utilizing the historic price-to-tangible e-book (“P/TB”) and price-to-earnings (“P/E”) multiples to worth Cambridge Bancorp. The inventory has traded at a median P/TB ratio of 1.38x prior to now, as proven under.

| FY20 | FY21 | FY22 | Common | |||

| T. Ebook Worth per Share ($) | 54.7 | 54.8 | 57.0 | |||

| Common Market Worth ($) | 60.3 | 84.8 | 84.5 | |||

| Historic P/TB | 1.10x | 1.55x | 1.48x | 1.38x | ||

| Supply: Firm Financials, Yahoo Finance, Creator’s Estimates | ||||||

Multiplying the typical P/TB a number of with the forecast tangible e-book worth per share of $62.6 provides a goal worth of $86.2 for the top of 2023. This worth goal implies a 29.4% upside from the March 24 closing worth. The next desk exhibits the sensitivity of the goal worth to the P/TB ratio.

| P/TB A number of | 1.18x | 1.28x | 1.38x | 1.48x | 1.58x |

| TBVPS – Dec 2023 ($) | 62.6 | 62.6 | 62.6 | 62.6 | 62.6 |

| Goal Worth ($) | 73.7 | 80.0 | 86.2 | 92.5 | 98.8 |

| Market Worth ($) | 66.7 | 66.7 | 66.7 | 66.7 | 66.7 |

| Upside/(Draw back) | 10.6% | 20.0% | 29.4% | 38.8% | 48.2% |

| Supply: Creator’s Estimates |

The inventory has traded at a median P/E ratio of round 11.5x prior to now, as proven under.

| FY20 | FY21 | FY22 | Common | |||

| Earnings per Share ($) | 5.03 | 7.69 | 7.30 | |||

| Common Market Worth ($) | 60.3 | 84.8 | 84.5 | |||

| Historic P/E | 12.0x | 11.0x | 11.6x | 11.5x | ||

| Supply: Firm Financials, Yahoo Finance, Creator’s Estimates | ||||||

Multiplying the typical P/E a number of with the forecast earnings per share of $8.29 provides a goal worth of $95.6 for the top of 2023. This worth goal implies a 43.4% upside from the March 24 closing worth. The next desk exhibits the sensitivity of the goal worth to the P/E ratio.

| P/E A number of | 9.5x | 10.5x | 11.5x | 12.5x | 13.5x |

| EPS 2023 ($) | 8.29 | 8.29 | 8.29 | 8.29 | 8.29 |

| Goal Worth ($) | 79.0 | 87.3 | 95.6 | 103.9 | 112.2 |

| Market Worth ($) | 66.7 | 66.7 | 66.7 | 66.7 | 66.7 |

| Upside/(Draw back) | 18.5% | 31.0% | 43.4% | 55.8% | 68.3% |

| Supply: Creator’s Estimates |

Equally weighting the goal costs from the 2 valuation strategies provides a mixed goal worth of $90.9, which suggests a 36.4% upside from the present market worth. Including the ahead dividend yield provides a complete anticipated return of 40.4%. Therefore, I’m sustaining a purchase ranking on Cambridge Bancorp.

[ad_2]