[ad_1]

Originally posted on inflationeducation.net:

The twond and threerd largest US financial institution failures of all time simply occurred, and there’s extra fireworks to come back. That is the predictable results of our centrally managed economic system, the place the Fed suppresses rates of interest inflicting wild hypothesis, solely to jack them as much as fight the inflation they brought on.

Growth, bubble, bust. Wash, rinse, repeat.

One of the crucial complicated classes in school economics is the inverse relationship between bond costs and bond yields. If rates of interest are increased, shouldn’t a bond be value extra? No, as a result of the comparability is to market charges, and a bond’s curiosity cost – or “coupon” – is fastened at issuance.

As prevailing market charges rise, present bond costs fall in order that their beforehand fastened coupon cost and redemption quantities match present maturity yields.

Fast instance: In mid-2020, 10-year US Treasury charges bottomed at 0.5%, so a $1,000 bond paid an annual coupon of $5, a whopping 5 simoleons to lend your Uncle Sam a grand.

Just lately although, because the Fed jacked up lending charges to combat inflation created by their very own easy-money coverage, the US 10-Yr yield hit 4%. Which means an annual coupon cost of $40.

The clincher?

What does that do to the market value of the 2020 Treasury with the $5 coupon? To match a 4% yield to maturity, it’s current worth should decline by over 20%.

That’s a giant loss on a supposed ‘risk-free’ asset. Bonds of every kind – company, municipal, even mortgages – endured comparable losses. And all these belongings are sitting on the steadiness sheets of banks, insurance coverage firms, and pension funds all over the place.

The result’s the banks now not have sufficient monetary belongings at at present’s costs to match liabilities. In easy phrases, there’s not sufficient cash to assist deposits.

If too many individuals withdraw – like It’s a Fantastic Life – the entire system goes up in flames.

Positive, Silicon Valley Financial institution (SVB) ought to have ‘hedged’ the rate of interest threat, however that simply means another person hiding the losses. It’s a large home of playing cards – everybody owes everybody else – and the unrealized losses triggered an old school financial institution run, one that may now transfer on the pace of sunshine.

The President, the Treasury Secretary, and the Federal Reserve Chair all panicked, stepping as much as assure deposits at ‘systemically necessary’ banks.

However this genius transfer (sarcasm alert!) was the sign for financial actors to withdraw from smaller banks that might not be thought-about ‘systemically necessary’.

In different phrases: Cue extra financial institution runs.

When the newest “Committee to Save the World” as they’ve really been known as by Time Journal (throughout earlier self-inflicted crises, as they bumble round feasting on the carcass of the US center class) figures this out, they’ll have to ensure depositor funds throughout the banking sector.

The result’s extra of the identical from 2008 – privatized income, socialized losses, ethical hazard encouraging dangerous conduct on the expense of taxpayers and forex holders.

Maybe extra related to your loved ones, this implies extra value inflation. Somewhat than marking the impaired belongings to market costs, they’re creating new cash from nothing to worth every little thing at par (in order that 2020 bond with a $5 coupon is marked to not $788, however proper again to $1,000).

In a single foul swoop, they’re undoing all makes an attempt to combat the inflation we’re seeing.

Worse, they’re choosing winners and losers, rewarding the well-connected with free cash whereas small companies, owners, and customers stay burdened with increased rates of interest.

This isn’t an America our forefathers would acknowledge.

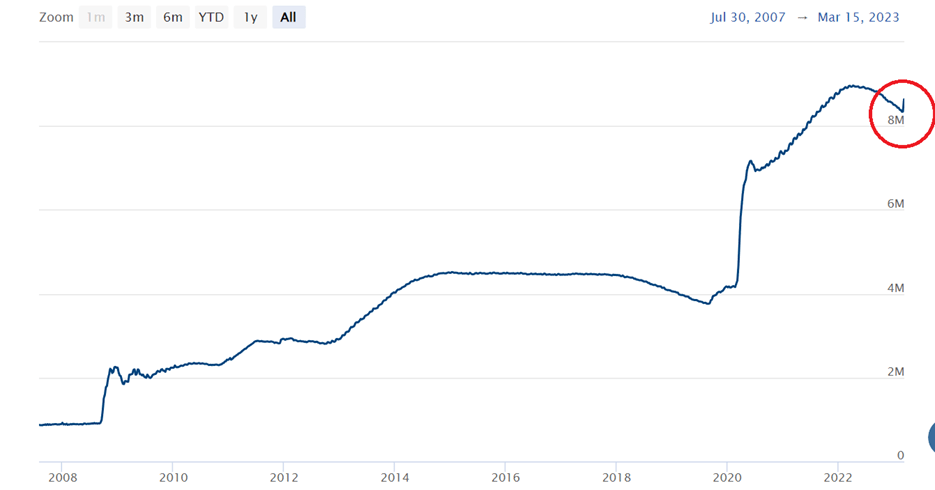

It’s plainly apparent: After they cease printing cash, our debt-based fiat cash system implodes. It’s a function, not a bug. Anticipate this development reversal in base cash to proceed upward like a hockey stick-

Supply: www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

That these clowns – Biden, Yellen, and Powell – might concurrently (a) maintain this a lot energy to destroy our economic system, crushing job and retirement prospects from Mount Excessive, and (b) not see any of this coming is, frankly, alarming. I’m a daily man and have been warning about it for years.

A good greater concern is that each one of this occurs in opposition to a geopolitical backdrop the place the BRICS nations (Brazil, Russia, India, China) together with the Center East, most of Asia and Africa, are collaborating on an alternate forex system to scale back dependence on the US Greenback.

The newest shoe to drop is the Saudi’s agreeing to just accept Chinese language yuan for oil, making a crack within the petrodollar backing that saved the US Greenback in 1974 (after we deserted gold-backing in 1971).

All of this implies a worldwide financial reset is coming; it might not be a sluggish and sustained inflation from predictable charges of money-printing. It could possibly be a tipping level that occurs shortly.

Client costs are pushed by two parts: (a) cash provide, and (b) cash velocity.

The latter is psychological, and nonlinear.

If confidence is misplaced by foreigners or a viable various is offered that isn’t shedding buying energy at 10% per yr, the flood of US {Dollars} again to American shores might grow to be a tsunami.

We’ll probably see the sign first in gold and silver, so watch these costs (and maintain some available as insurance coverage). Bitcoin, too, is a pleasant hypothesis that would function an escape valve (self-custodied).

Is Capitalism failing?

No, expensive buddies, capitalism is just not failing. There are not any authorities bailouts in capitalism. There’s no such factor as ‘too large to fail’. Stuffed shirts in DC don’t get to choose winners and losers.

True capitalism would require an abolishment of the Federal Reserve. The value of cash – rates of interest – ought to be set in free markets, between debtors and lenders.

What’s failing us at present is a damaged, crooked, debt-based fiat cash system in its dying throws, a large beast thrashing round on it’s deathbed, crushing every little thing in sight earlier than it goes limp.

In abstract, the Fed brought on this disaster by reducing charges and printing cash, enriching the wealthy, encouraging borrowing, and inflicting wild hypothesis – the ‘every little thing bubble’. When this lastly brought on client costs to rise, they raised charges and broke the banking system, stuffed to the gills on all of the debt-issuance. That’s now risking widespread financial institution runs and systemic failure.

They don’t have the abdomen for that, so the outcome shall be extra inflation.

[ad_2]