[ad_1]

Over the previous 90 years, the general public has ceaselessly been warned that the US funds deficit would result in an financial disaster. As within the well-known story concerning the boy who cried wolf, they finally started to tune out these warnings. And it does no good to quote particular knowledge concerning the funds deficit rising to a whole lot of billions and even trillions of {dollars}; these figures haven’t any which means to common individuals. I think that if you happen to polled individuals on the implications of a $800 million deficit and a $800 billion greenback deficit, the solutions could be related.

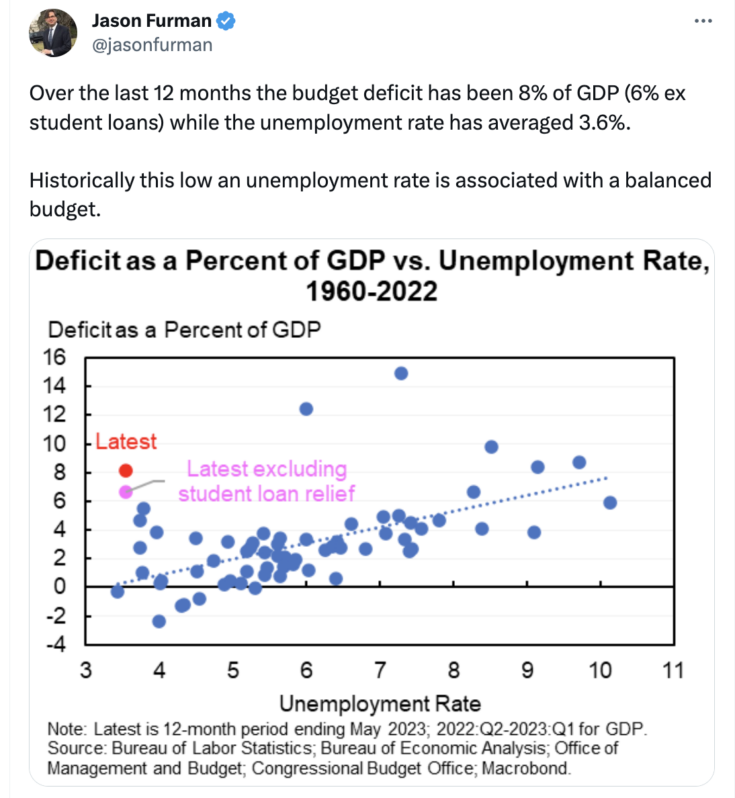

However this time is totally different, as one thing vital has modified. The wolf isn’t but on the door, however it’s getting nearer. Over the previous 5 years, the US funds deficit has shifted to a extra unsustainable path. Matt Yglesias directed me to this tweet by Jason Furman:

The dotted line is upward sloping as a result of deficits are sometimes worse during times of excessive unemployment, which is correctly. The additional above the dotted line, the extra out of line the deficit, given the situation of the enterprise cycle.

Again in 2019, I argued that US fiscal coverage was essentially the most reckless in US historical past. It’s not that the funds deficit was all that prime (4.6% of GDP), moderately it was unusually excessive on condition that unemployment was close to an all-time low. I knew that issues would develop into far worse within the subsequent recession, though I didn’t know that the recession would come so quickly.

I stand by my declare that (on the time) 2019 fiscal coverage was essentially the most reckless in American historical past, despite the fact that every of the following 4 years ended up being much more reckless. When it comes to vertical distance above the dotted line, 2020 was the very worst, then 2021, then 2023 (estimated—pink dot), then 2022, after which 2019 (roughly tied with 2009.)

The consequence of the reckless fiscal coverage is not going to be a monetary disaster. Nor will it’s a default. Even the everlasting monetization of the debt is unlikely, in my opinion. The almost definitely consequence will probably be larger future taxes and slower financial progress. This can result in lowered residing requirements. It may additionally push politics in a extra “populist” course, with penalties which might be tough to foretell (however unlikely to be fascinating.)

P.S. The excellence between larger taxes and decrease spending is much less clear than you would possibly assume. Thus one possibility is a $1000 tax enhance on wealthy individuals. An alternative choice is a $1000 lower in Social Safety advantages for wealthy individuals. The primary represents larger taxes whereas the second is decrease spending. However the penalties for implicit marginal tax charges are fairly related.

[ad_2]