[ad_1]

I used to be at all times a saver rising up.

Every time I obtained cash for birthdays, holidays, church stuff, my allowance, or summer time jobs, I might sock it away. At first that was in a secret compartment in a pockets within the high drawer of my dresser.

In highschool, I lastly opened up my first checking account. My first job was as a bus boy. I in all probability saved a thousand {dollars} that summer time. The following summer time I delivered furnishings and saved a bit extra.1

After 17 years or so of saving I had just a few thousand {dollars} saved up so my dad and I went over some money administration choices on the native financial institution the place my cash was simply sitting in a checking account.

CD charges have been increased than they have been paying on a financial savings account in order that made sense. I believe it paid one thing like 5% over 12 months.

I put just a few thousand bucks into that CD with the concept that it will mature as I used to be going away to school. A yr later I collected my cash together with a bit little bit of curiosity.

Is that this probably the most boring first funding story in historical past? Most likely. Too sensible for an adolescent? Most actually.2

However I had no information in anyway of the inventory market at that time and my time horizon was so brief {that a} boring previous certificates of deposit made probably the most sense for my threat profile.

This was again within the late-Nineteen Nineties so CD charges have been a lot increased than they’ve been for almost all of this century.

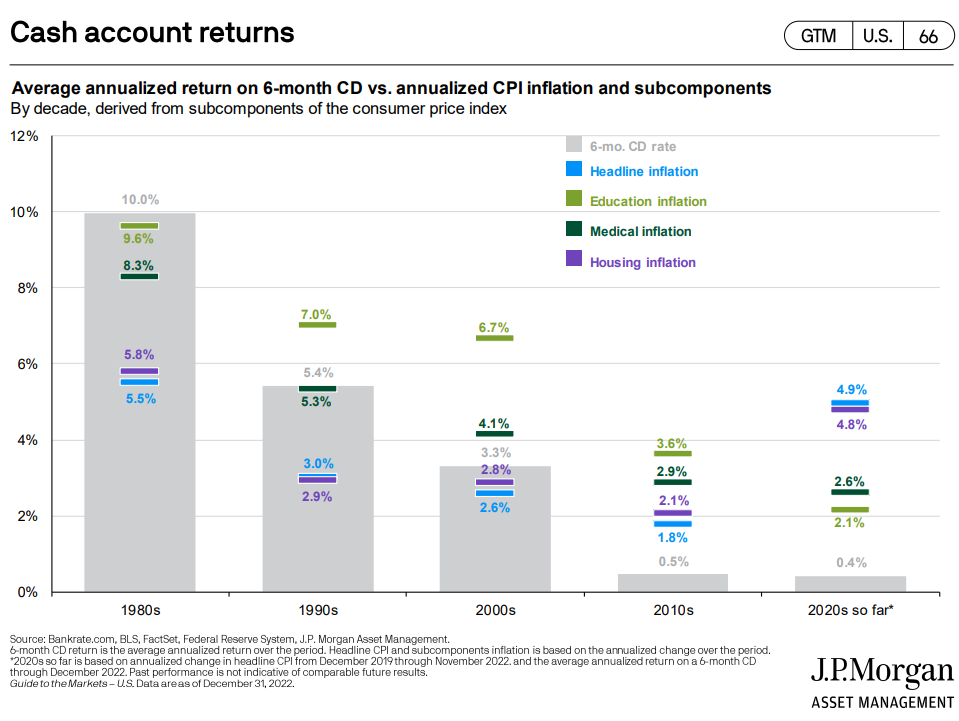

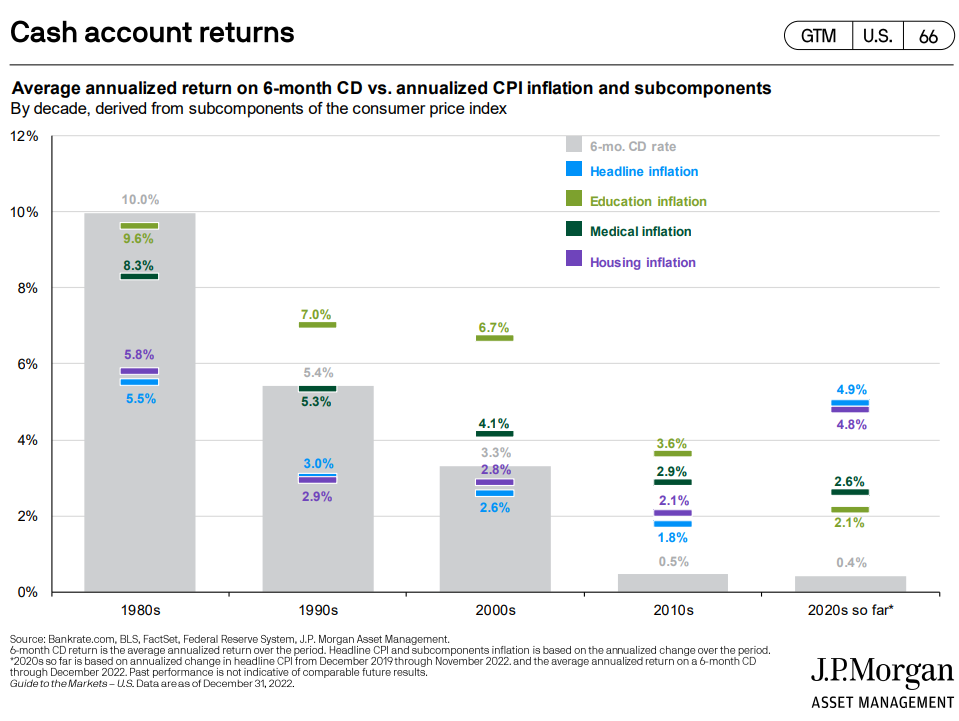

JP Morgan has a chart that compares common 6-month CD charges by decade together with some completely different measures of inflation:

It’s laborious to consider common CD charges within the Eighties have been increased than the inflation price. It was a stairstep down from there with common charges close to the bottom flooring degree by the 2010s. Common charges for the 2020s aren’t any higher however the charges in the present day have lastly reached the respectable ranges I used to be getting after I made my first CD buy.

Savers have taken discover.

The Wall Street Journal had a chunk out lately detailing the massive move of capital in CDs:

Excessive inflation, rising rates of interest, and financial nervousness are making CDs cool once more, with yields rising as excessive as 5.25% lately at some banks. Balances in CDs rocketed from $36.5 billion in April 2022 to $418.4 billion in January, in keeping with the Federal Reserve.

The typical yield on a 12 month CD remains to be simply 1.6% but when you realize the place to look (simply search among the on-line banks) you will get one thing within the vary of 4% to five% proper now.

The speed is dependent upon the supplier and your time horizon.

I pulled up the CD charges for Ally Bank this morning. A 12-month CD was quoted at 4.5% however exit to 18 months and it was 5%. Nevertheless, 3 and 5 yr charges have been 4.25%. Go shorter and charges have been decrease (2% annualized for 3 months).

There are professionals and cons to CDs.

On the constructive facet of issues, locking in 5% short-term charges takes among the rate of interest volatility out of the equation if the Fed is compelled to chop charges if they assist trigger extra ache within the financial system or banking system (or each).

It’s additionally good to have an finish date in thoughts in case you’re planning on utilizing the cash at a sure level sooner or later.

One of many greatest downsides of CDs is you surrender liquidity to lock in these yields. Most banks will allow you to pull your cash early however there may be sometimes a penalty within the type of misplaced curiosity.

Alternatively, locking up your cash does take among the temptation away from continually tinkering together with your money.

I’m undecided how lengthy in the present day’s CD charges will final. Quick-term bond yields have come down fairly a bit in latest weeks in order that could possibly be a precursor to decrease charges sooner or later. Or possibly the bond market is simply as confused as everybody else proper now.

I don’t know the longer term path of rates of interest from right here so I’m not going to faux I do.

However I might benefit from the yields we have now on CDs proper now as a result of they won’t final very lengthy.

Michael and I talked concerning the first investments we ever made and way more on this week’s Animal Spirits video:

Subscribe to The Compound so that you by no means miss an episode.

Additional Studying:

More Money Doesn’t Make Make You Better at Managing Your Finances

Now right here’s what I’ve been studying these days:

1Not a enjoyable job in any respect however lifting all these heavy sleeper sofas, dressers and sectionals did assist maintain me in form.

2My funding type is so boring my second funding was an IRA contribution right into a targetdate fund. Sorry not sorry.

[ad_2]